Cambodia Investment Review

Cambodia could unlock billions of dollars in new lending capacity and accelerate economic growth by reforming the way distressed debt is resolved, according to a new report from Mekong Strategic Capital, which argues that lengthy debt resolution processes have become a growing drag on the economy.

While rising non-performing loans (NPLs) have attracted increasing attention from investors and policymakers in recent years, the report contends that Cambodia’s challenge is not simply the volume of bad loans within the banking system, but the amount of time required to resolve them.

According to the analysis, the country’s financial sector remains relatively resilient despite a sharp increase in distressed loans. Banks have built significant provisions against potential losses, maintain substantial capital buffers and continue to generate profits.

Instead, the report argues that unresolved debt is tying up capital, prolonging weakness in the property sector and limiting the ability of financial institutions to support new economic activity.

“The issue is not simply how many loans have become distressed. It’s how long those loans remain unresolved,” said Stephen Higgins, Managing Partner of Mekong Strategic Capital.

“The longer assets remain tied up in the system, the greater the drag on economic growth.”

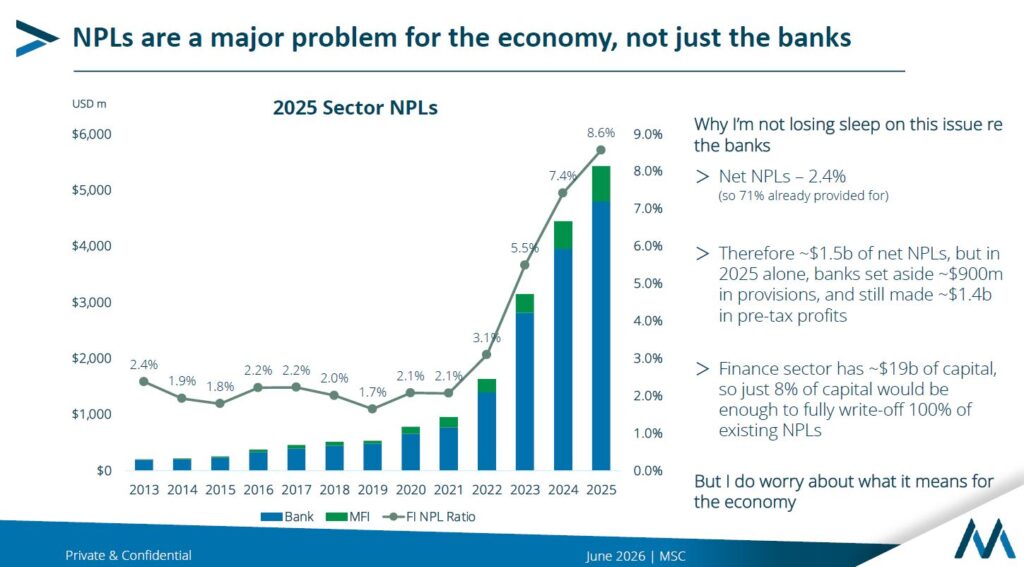

Distressed Debt Continues to Build

The report estimates that approximately $12.7 billion worth of loans are either more than 30 days overdue or have undergone restructuring, representing around 20 percent of total loans in Cambodia’s financial system and roughly one-quarter of national GDP.

Loan arrears have risen significantly during the opening months of 2026, which the report attributes to a combination of factors including higher fuel prices, disruptions linked to the Thai border situation, the government’s crackdown on online scam operations and a reduction in loan restructuring activity compared with 2025.

Much of this debt is secured by real estate assets, creating broader implications for Cambodia’s property market.

According to the report, distressed assets that remain unresolved for years contribute to what economists often describe as a property market overhang, where investors delay purchases in anticipation of future distressed sales while assets remain tied up in lengthy legal and recovery processes.

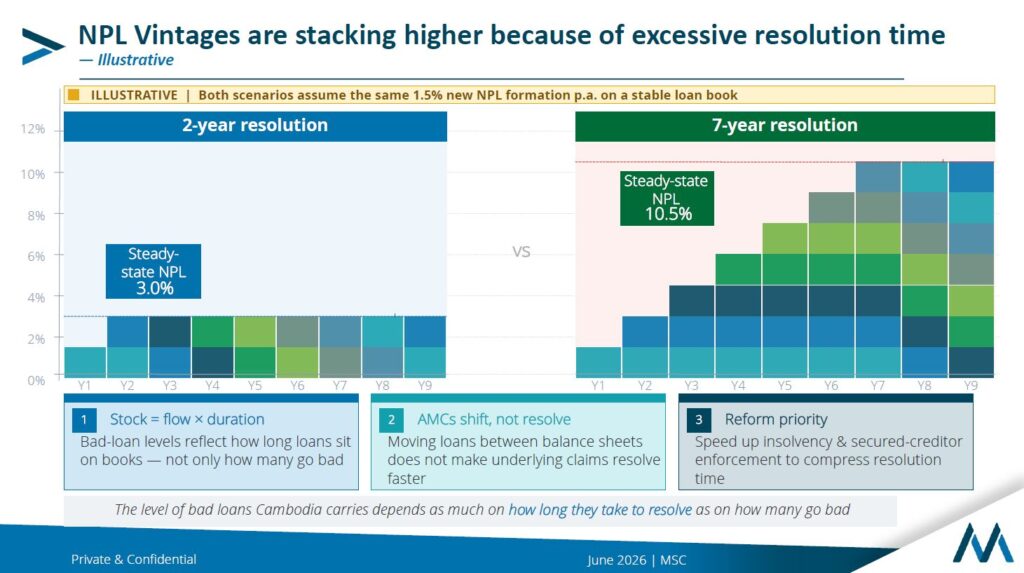

The Real Issue May Be Resolution Time

A key argument presented by Mekong Strategic Capital is that the level of bad loans in an economy depends not only on how many loans become distressed, but also on how quickly those loans can be resolved.

Using an illustrative example, the report estimates that a financial system resolving distressed loans within two years could maintain a steady-state NPL ratio of approximately 3 percent. However, if resolution periods stretch to seven years, the same rate of new bad-loan formation could result in an NPL ratio exceeding 10 percent.

“The concern is less about the stability of banks and more about what prolonged resolution means for borrowers, investors and economic growth,” Higgins said.

“Every year a distressed loan remains unresolved, value is lost. Assets deteriorate, debt burdens increase and capital that could be supporting new businesses remains trapped.”

The report also argues that simply transferring distressed loans between institutions or asset management companies does not solve the underlying problem if legal and insolvency processes remain slow.

Banks Appear Capable of Managing Current Losses

Despite concerns about rising NPLs, the report notes that Cambodia’s banking system remains well-capitalised.

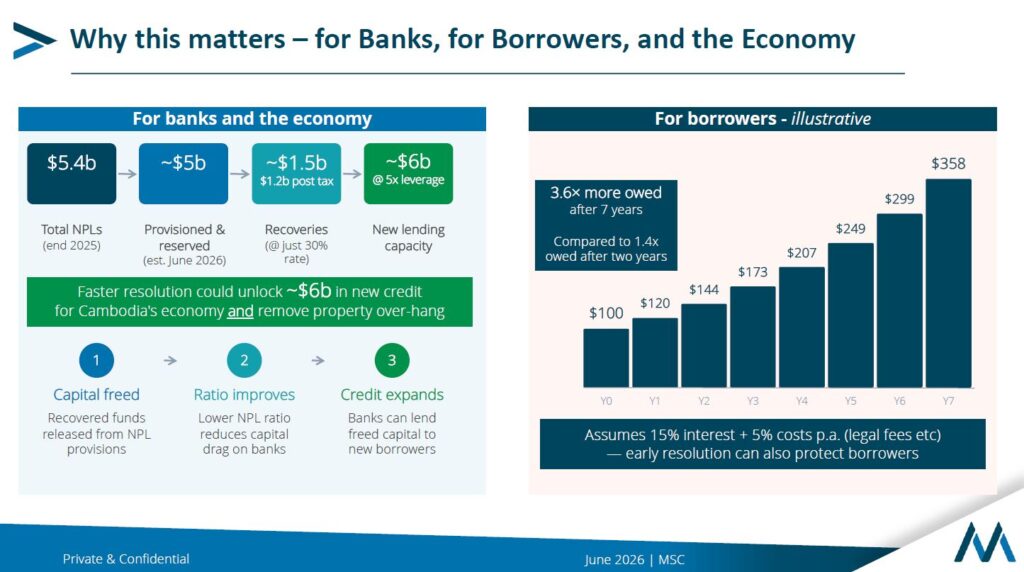

Sector-wide NPLs reached approximately $5.4 billion at the end of 2025, while net NPLs stood at around 2.4 percent after provisions, indicating that a substantial portion of potential losses has already been recognised by financial institutions.

Banks reportedly set aside roughly $900 million in provisions during 2025 while still generating around $1.4 billion in pre-tax profits. The report estimates that the financial sector holds approximately $19 billion in capital, providing significant capacity to absorb existing losses if necessary.

As a result, the report suggests the larger economic challenge lies in ensuring distressed assets can be recycled back into productive use rather than remaining trapped within the financial system.

Reform Could Unlock New Growth

Mekong Strategic Capital estimates that faster resolution of distressed loans could unlock as much as $6 billion in new lending capacity for Cambodia’s economy. Recoveries would release capital currently tied up in provisions, improve balance sheets and support additional lending to businesses and households.

The report calls for reforms aimed at accelerating insolvency proceedings and secured-creditor enforcement, while also introducing a personal insolvency framework that would provide households with a structured path to address unsustainable debts.

According to Higgins, creditor rights and borrower protections should be viewed as complementary rather than competing objectives.

“Faster resolution benefits everyone,” he said. “It helps banks recycle capital, helps borrowers find a path forward and helps the economy by putting money back to work.”

For investors, the report’s central message is that Cambodia’s next phase of financial sector reform may be less about banking stability and more about improving the legal and institutional mechanisms needed to resolve distressed debt efficiently.

If successful, such reforms could play a critical role in supporting credit growth, reducing pressure on the property market and strengthening the foundations for Cambodia’s long-term economic development.