By Suon Mach

Central banks around the world share a common and fairly straightforward mission: to keep prices stable, support long-term economic growth, and, where possible, help people stay employed. To guide this balancing act, institutions like the Federal Reserve and the European Central Bank have settled on a 2 percent inflation target as a key benchmark.

This is not just a technical goal. It plays a quiet but powerful role in shaping expectations. When people believe inflation will remain low and predictable, they are more likely to spend, save, and invest with confidence, which in turn helps keep the broader economy steady.

A major part of a central bank’s job is also to avoid deflation, which occurs when prices fall continuously and economic activity begins to stall. At first glance, falling prices may seem beneficial for consumers, but in reality, deflation can be deeply damaging.

If people expect prices to keep dropping, they tend to delay purchases. This reduces demand, slows production, and can ultimately lead to job losses. A modest and positive inflation rate of around 2 percent acts as a buffer against this risk. It keeps money circulating through the economy and helps prevent a downward spiral that can be extremely difficult to reverse once it takes hold.

Measurement challenges also help explain why central banks aim for a target above zero. Inflation is typically tracked using the Consumer Price Index (CPI), but it is not a perfect measure. It can sometimes overstate true inflation because it struggles to fully capture improvements in product quality or the introduction of new goods and services.

For instance, a smartphone today may cost the same as one from several years ago, yet it offers far more features and performance. By targeting 2 percent instead of zero, central banks build in a margin of safety. This reduces the risk of unintentionally slipping into negative inflation while still maintaining a credible and transparent policy framework.

Why a Little Inflation Helps Keep People in Their Jobs

The labor market adds another layer of complexity. Central banks are not only concerned with prices but also with employment and income stability.

One well-known issue is that wages tend to be “sticky” downward, meaning employers are often reluctant to cut nominal wages even during economic downturns. Moderate inflation helps ease this constraint. It allows real wages, adjusted for inflation, to change gradually without requiring outright pay cuts.

As a result, businesses are better able to retain workers, and sharp increases in unemployment can be avoided when the economy slows.

Another important reason behind the 2 percent target is the need for policy flexibility. Central banks primarily use interest rates to manage economic cycles. They raise rates to control inflation and lower them to stimulate growth during slowdowns. If inflation is too low, interest rates can drift dangerously close to zero, leaving policymakers with limited room to respond when a recession occurs.

A slightly higher inflation environment helps keep interest rates above zero during normal times. This gives central banks the space they need to cut rates when necessary, which becomes especially important during economic crises.

The 2 percent target did not emerge from a precise scientific formula. Instead, it has practical origins. The idea first gained traction during policy discussions at the Reserve Bank of New Zealand in the late 1980s. From there, it gradually spread to other countries and eventually became a global standard. Over time, it proved to be a useful focal point for communication and credibility, even though economists generally agree that there is nothing inherently special about the number itself.

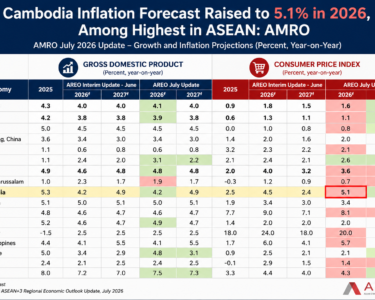

Why Cambodia Needs a Flexible Inflation Range

For Cambodia, applying a strict 2 percent target is not so straightforward. The country’s highly dollarized economy, in which the U.S. dollar is widely used alongside the local currency, limits the central bank’s ability to fully control monetary conditions.

This makes it more difficult to manage inflation in the same way as larger and more self-contained economies. In this context, a flexible inflation range may be more practical than a fixed target.

Strengthening the use of the riel, deepening the financial system, and improving monetary policy tools could all contribute to a more stable economic environment. In fact, a slightly higher but stable rate of inflation may better support growth, investment, and resilience in Cambodia’s evolving economy.

Despite ongoing debates and changing global conditions, most central banks continue to rely on the 2 percent benchmark.

One reason is continuity, as it is a target that markets understand and trust. That credibility matters because when people believe central banks will follow through on their commitments, it helps anchor expectations and reduce uncertainty.

Ultimately, the 2 percent target is not about achieving a perfect number. It is about maintaining stability, building confidence, and ensuring that policymakers have the tools they need to respond effectively when economic conditions shift.

Suon Mach is a second-year master’s degree student in Development Studies at the Royal University of Phnom Penh.