Cambodia Investment Review

Cambodia’s banking sector is entering what industry leaders describe as a defining period of adjustment rather than a systemic crisis, with strong capital buffers, ample liquidity and close regulatory oversight helping underpin confidence despite rising concern fuelled by rumours, social media speculation and a more challenging credit environment.

That was the central message emerging from the recent Annual General Meeting of the Association of Banks in Cambodia (ABC), where Chairman Rath Sophoan said the Kingdom’s financial system remains fundamentally sound, even as lenders navigate slower credit growth, elevated non-performing loans and weaker sentiment in parts of the market.

Read More: Association of Banks in Cambodia Re-Elects Rath Sophoan as Chairman for 2026–2028 Term

Sharing the background information with Cambodia Investment Review, the association also outlined key sector data showing that while Cambodia’s banking industry is under pressure from economic headwinds and misinformation, the broader system remains well-capitalised, liquid and closely supervised by the National Bank of Cambodia (NBC).

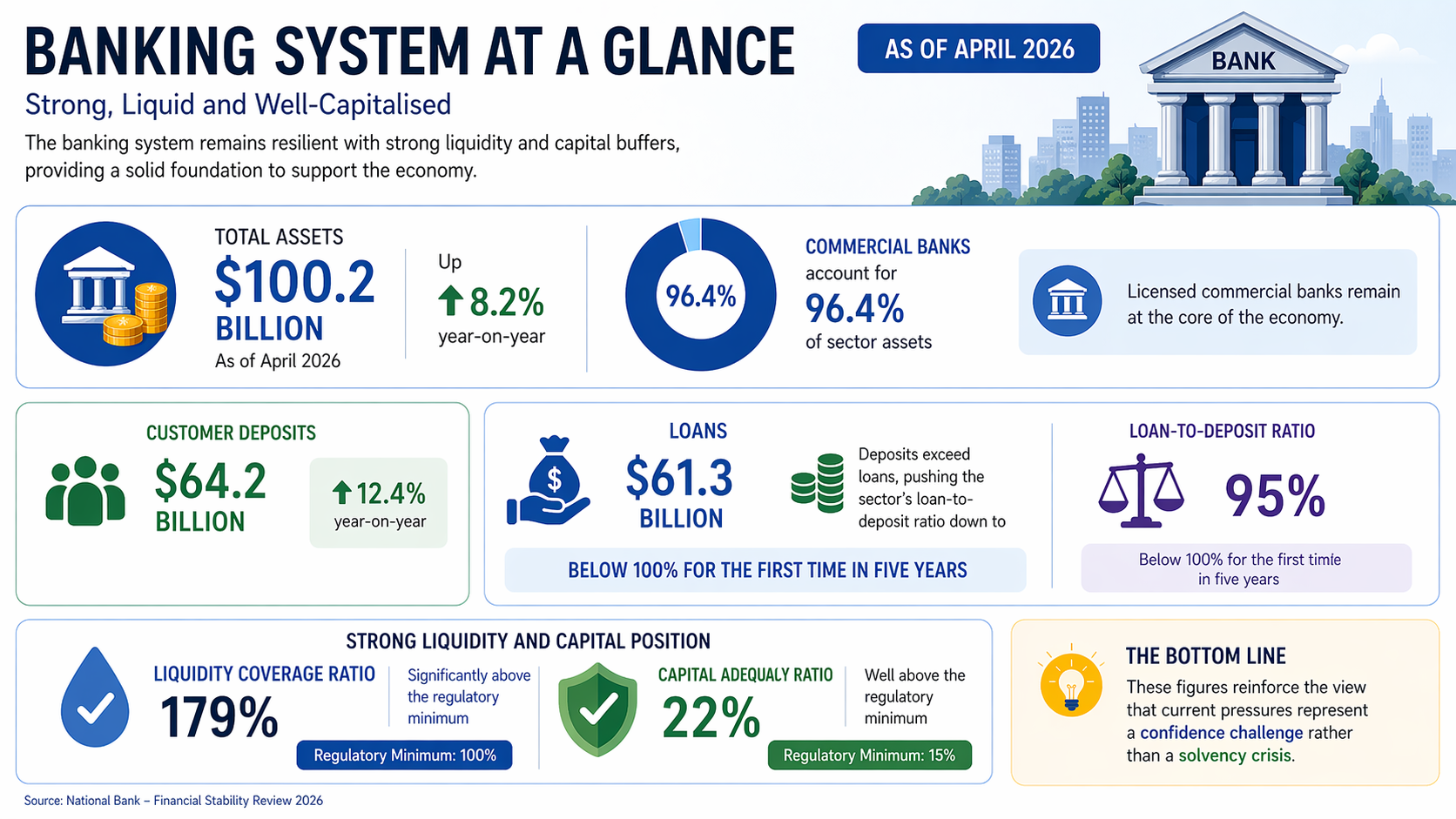

A $100 Billion Financial System Still Standing Firm

Cambodia’s banking system assets grew of approximately $100.2 billion by end of 2025, up around 8.2% year-on-year, according to NBC’s Financial Stability Review 2025. Commercial banks alone accounted for 96.4% of sector assets, highlighting the continued central role of licensed banks in Cambodia’s economy.

Customer deposits reached $64.2 billion, rising 12.4% year-on-year, while the total number of depositors climbed to 18.6 million. Loans stood at $61.3 billion, meaning deposits exceeded loans and pushed the sector’s loan-to-deposit ratio down to 95% — below 100% for the first time in five years.

For banking analysts, that matters.

It suggests institutions are not overextended and that liquidity conditions remain relatively comfortable. In practical terms, the system holds more customer funding than outstanding loans, providing a stronger base to absorb volatility.

At the same time, Cambodia’s commercial banks were estimated to hold a Liquidity Coverage Ratio of around 179%, significantly above the regulatory minimum of 100%, while capital adequacy ratios for deposit-taking institutions stood at 22%, well above the 15% minimum.

These figures reinforce the ABC’s view that current pressures represent a confidence challenge rather than a solvency crisis.

Association of Banks in Cambodia (ABC) Chairman Rath Sophoan

The Real Challenge: Asset Quality and Slower Growth

Still, the sector is not without problems.

The gross non-performing loan (NPL) ratio rose to 8.3% in 2025, the highest level in a decade, while deposit-taking banks and financial institutions restructured loans for a total of $5.65 billion across more than 207,830 accounts. Provision coverage declined to 67.5%, down from 73.5% a year earlier.

That means banks are carrying a heavier burden from stressed borrowers, particularly after years of pandemic disruptions, a slower property market and softer household demand.

Speaking at the AGM, Rath Sophoan acknowledged that profitability has moderated due to higher provisioning and rising funding costs, but stressed that institutions remain stable and well-capitalised.

“This resilience is not accidental,” he said. “It reflects strong governance, responsible lending practices, and close collaboration between regulators and industry participants.”

The ABC has also identified slower recovery in real estate and construction, pressure on loan quality, illegal lending and rising cybersecurity risks as key challenges facing members over the next phase.

Social Media Rumours Put Trust to the Test

Recent public concern surrounding isolated banking developments and false online claims has shown how quickly sentiment can shift in a digitally connected economy.

A recent joint statement by the ABC and Cambodia Microfinance Association warned against false claims regarding supposed U.S. action against Cambodian banks, calling on the public to rely only on verified information from official regulators and licensed institutions.

While rumours alone do not weaken balance sheets, they can create unnecessary anxiety among depositors and businesses if left unchecked.

That is why confidence has become one of the sector’s most valuable assets.

The ABC’s own internal messaging frames the current environment around a simple principle: trust is the new capital.

Both the NBC and industry associations have increasingly adopted coordinated public communication strategies aimed at maintaining transparency while discouraging misinformation.

According to briefing materials shared with CIR, the NBC has also issued statements addressing public concerns, delicensed institutions that failed to meet requirements, and continues work on emergency liquidity assistance tools, asset management institution frameworks and a future deposit guarantee scheme.

Long queues formed outside the Head Office branch of APD Bank in the Phnom Penh City Centre after social media rumor.

Digital Payments Become a Major Strength

Another bright spot is Cambodia’s rapidly evolving payments ecosystem.

The Bakong payment system processed 1.3 billion transactions in 2025, up 118.7% in volume, with total transaction value reaching KHR 899.1 trillion — equivalent to around 4.5 times GDP.

Cross-border Bakong transaction value rose 235.3%, while the riel share of Bakong payments climbed to 58.2%, supporting Cambodia’s broader de-dollarisation strategy.

Meanwhile, mobile and internet banking transactions combined were estimated at around six times GDP in value, underscoring how digital infrastructure is becoming one of Cambodia’s strongest banking assets.

For lenders, this presents an opportunity to offset slower traditional lending growth through payments, digital products, SME finance and operational efficiency.

Where Growth May Come Next

At the AGM, Rath Sophoan said Cambodia’s banking sector remains well positioned to support the country’s long-term economic ambitions, particularly under the government’s Pentagonal Strategy.

He pointed to trade finance, supply chain finance, manufacturing, agriculture modernisation, healthcare and education as sectors with strong potential for responsible credit expansion.

That shift is important.

After years of heavy exposure to property-linked sectors, many banks are now expected to diversify portfolios toward productive industries tied to exports, domestic consumption and formalisation of the wider economy.

Manufacturing FDI inflows and improving tourism trends may also help create healthier lending demand than speculative asset cycles of the past.

Confidence Test, Not Crisis

For investors, businesses and depositors, the immediate takeaway is clear: Cambodia’s banking sector is under pressure, but it is not in systemic distress.

The industry is adjusting to slower growth, tighter credit discipline and the unwinding of post-pandemic support measures. Some institutions will perform better than others, and consolidation may continue. But the system overall retains strong liquidity, significant capital buffers and an active regulator.

In many ways, 2026 may prove less about financial weakness and more about whether institutions can maintain trust while modernising their business models.

As the ABC put it in materials shared with CIR, this is a defining transition — not a crisis.