Cambodia Investment Review

Cambodia’s small business credit market showed signs of slowing momentum in the first quarter of 2026, with overall loan application growth remaining largely flat and construction-related borrowing continuing to decline, according to the latest Small Business Credit Index released by Credit Bureau Cambodia (CBC).

The report, which tracks small business credit demand, loan performance, and portfolio quality across Cambodia’s financial sector, showed that the overall number of small business credit applications increased by just 1 percent quarter-on-quarter during the January to March 2026 period.

While overall application volumes remained stable, the total value of small business credit applications fell by 5.1 percent quarter-on-quarter, suggesting more cautious borrowing behavior among Cambodian consumers and small business operators.

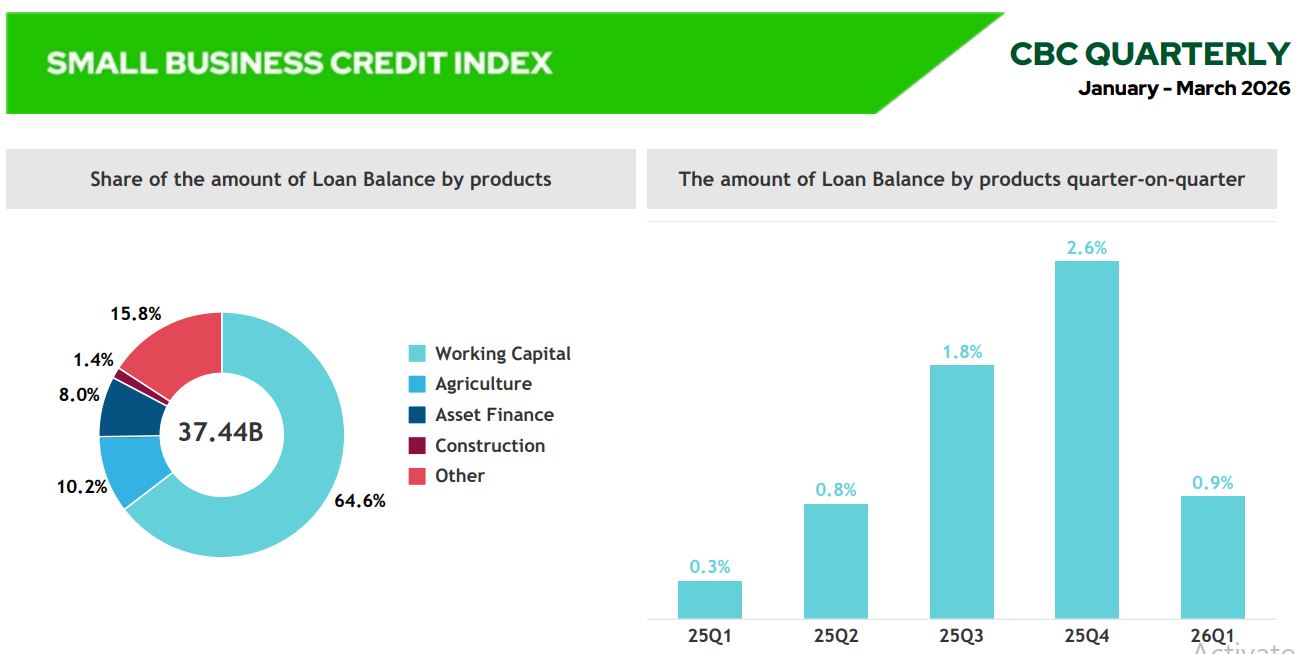

Working capital loans continued to dominate the market, accounting for 70.5 percent of total credit applications by number and 78.1 percent by value, highlighting continued demand for operational financing among businesses navigating softer economic conditions.

Agriculture and Asset Finance Show Resilience

Despite the broader slowdown, agriculture-related loan applications rose 18.2 percent quarter-on-quarter, while asset finance applications increased 3.8 percent, indicating continued investment activity in productive sectors.

Construction lending, however, remained under pressure, with construction-related credit applications declining 18.5 percent quarter-on-quarter, reflecting ongoing weakness in Cambodia’s property and construction sectors.

Regionally, the Plateau area recorded the strongest increase in credit applications at 13.4 percent, while the Coastal and Plain regions both saw declines. Agriculture financing in the Plateau region surged 73.5 percent quarter-on-quarter, one of the strongest sectoral increases recorded in the report.

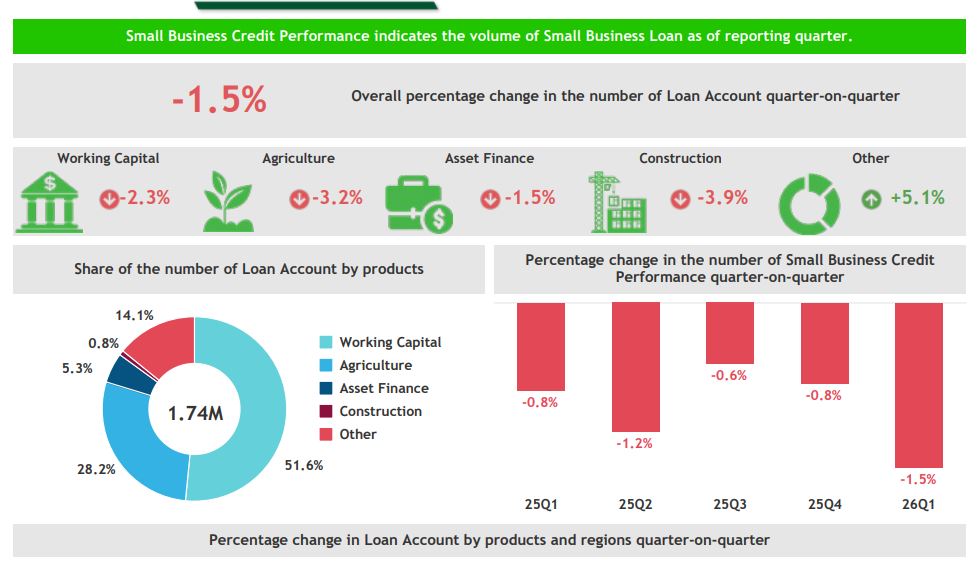

CBC’s data also showed that the total number of active small business loan accounts fell 1.5 percent quarter-on-quarter to 1.74 million accounts, extending a trend of softer lending activity seen throughout 2025.

Working capital loans represented 51.6 percent of all outstanding loan accounts, followed by agriculture at 28.2 percent. Construction-related loan accounts declined 3.9 percent during the quarter.

Loan Balances Continue to Grow

Although the number of loan accounts declined, the overall balance of small business loans continued to rise, increasing 0.9 percent quarter-on-quarter to $37.44 billion.

Asset finance balances recorded some of the strongest growth across regions, particularly in the Coastal region where balances increased 17.3 percent quarter-on-quarter.

The report suggests that while fewer borrowers may be taking out loans, average loan sizes and refinancing activity remain relatively elevated in certain sectors.

CBC also highlighted ongoing credit quality concerns across Cambodia’s small business sector.

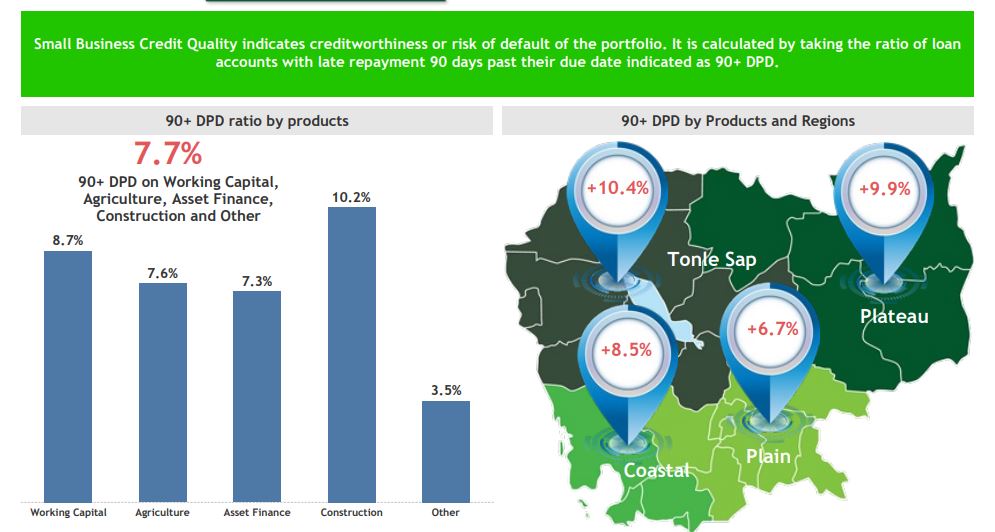

The overall 90+ days past due (90+ DPD) ratio for small business loans stood at 7.7 percent during the quarter, with construction loans recording the highest delinquency rate at 10.2 percent. Working capital loans followed at 8.7 percent, while agriculture loans stood at 7.6 percent.

Credit Quality Remains Under Pressure

The Tonle Sap region recorded the highest 90+ DPD ratio at 10.4 percent, followed by the Plateau region at 9.9 percent.

CBC’s report also showed that 30.3 percent of borrowers maintained relationships with multiple financial institutions, while 55.3 percent of borrowers held only one loan account.

Credit Bureau Cambodia said the quarterly index is designed to provide insights into the country’s small business credit market using data submitted by financial institutions across the Kingdom. The index covers three core components: credit applications, credit performance, and credit quality.

*In the CBC report, a “small business loan” does not necessarily mean a formal SME corporate loan taken out by a registered company.

CBC defines it as a consumer loan that is being used for business purposes. In Cambodia, a large portion of SMEs and microbusinesses borrow under personal names rather than through formal company structures, so CBC tracks these as “small business credit.”