Cambodia Investment Review

Cambodia’s property market entered 2026 with a mixed but gradually improving outlook, as stronger demand for affordable housing contrasted with softer office and retail leasing conditions, according to the Cambodia Q1 Real Estate Outlook 2026 released by Advantage Property Services.

The report suggests the Kingdom’s real estate sector is moving into a more disciplined phase of recovery, where pricing, quality, location and end-user demand are increasingly driving performance rather than speculative investment. While new projects continue to launch across several segments, occupiers and buyers are becoming more selective amid tighter financing conditions and broader economic uncertainty.

Affordable Housing Continues to Lead Residential Demand

Phnom Penh’s residential market showed the clearest signs of momentum in the first quarter, particularly in affordable and mid-range condominium developments aimed at local buyers.

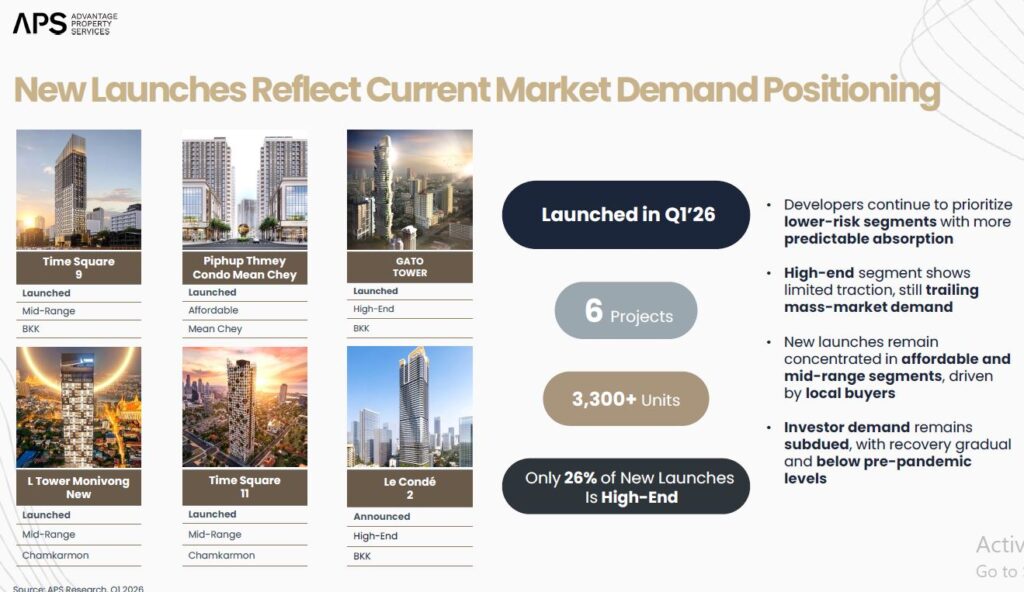

APS reported that more than 3,300 condominium units were launched in Q1 2026 across six projects. Only 26% of those launches were in the high-end category, reflecting continued caution among developers toward luxury inventory and stronger confidence in price-sensitive segments.

The capital now has more than 76,000 condominium units across over 150 projects, with mid-range developments accounting for the largest share of market supply. APS said developers are increasingly targeting owner-occupiers and domestic households seeking practical housing options, while investor demand remains below pre-pandemic levels.

New completions during the quarter also leaned heavily toward affordable projects, reinforcing the shift toward real demand rather than speculative buying. The report noted that payment flexibility, livability and location remain major decision factors for today’s buyers.

Office Market Expands as Tenants Become More Selective

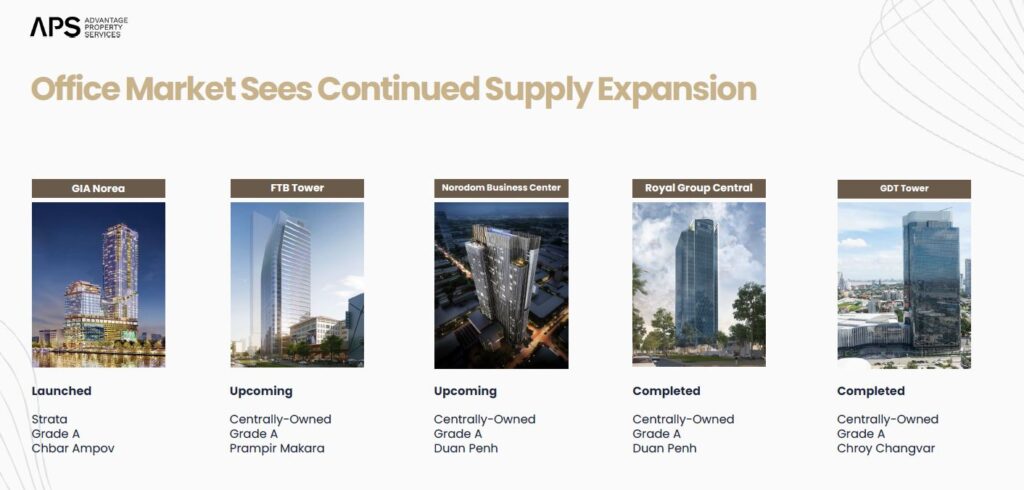

Phnom Penh’s office sector continued to grow, with a new wave of Grade A towers adding pressure to an already competitive leasing environment.

APS forecasts total office stock could reach around 1.3 million square meters in 2026, supported by more than 144,000 square meters of expected new supply this year.

Despite the incoming space, premium buildings continued to outperform. Grade A occupancy improved quarter-on-quarter, while lower-tier buildings saw weaker leasing conditions, particularly in the CBD and non-core districts.

The report said tenants are increasingly prioritizing quality buildings with stronger ownership profiles, better maintenance standards and practical amenities such as food courts, parking access and breakout areas. In some cases, companies are using softer market conditions to relocate into better offices without significantly increasing costs.

Rental pressure remained concentrated in Grade B and Grade C buildings, where landlords face greater competition and more aggressive negotiations from tenants.

Retail Conditions Diverge Between Malls and High Streets

Cambodia’s retail market also showed a split recovery in Q1, with traditional malls facing pressure while prime street-front locations remained more resilient.

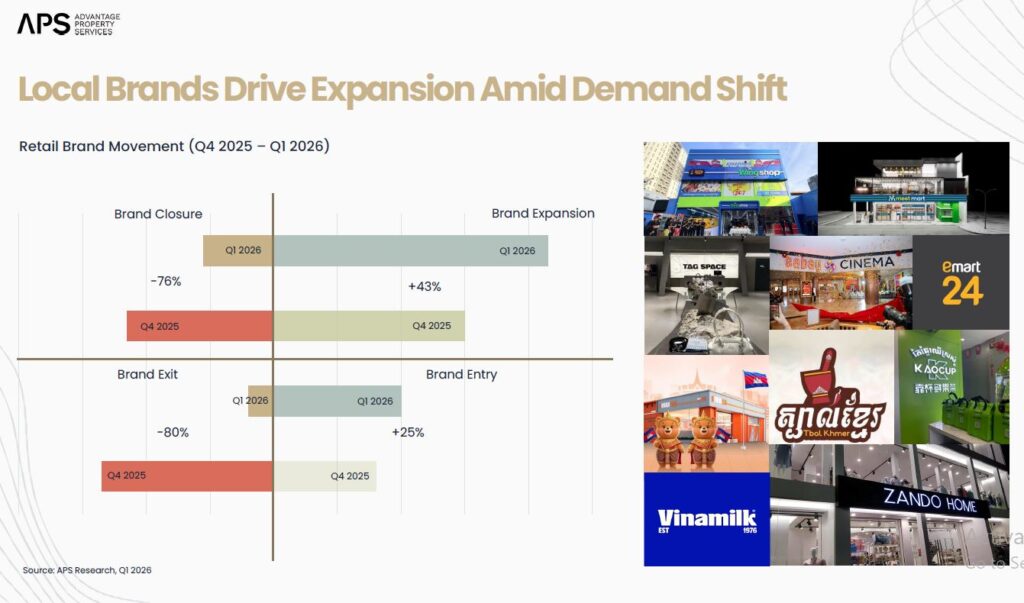

APS said Phnom Penh retail occupancy fell to 56.8% during the quarter as new supply entered the market and some tenants exited underperforming centers. Community malls and older formats were among the most exposed to softer demand.

By contrast, prime high street locations recorded rental growth, supported by stronger foot traffic, tourism activity and continued interest from food and beverage operators.

The report noted that Cambodian-owned brands, convenience chains and standalone retail concepts are becoming increasingly visible in the market, particularly in newer lifestyle districts and mixed-use destinations such as Koh Pich and Koh Norea.

This suggests retail demand is not disappearing, but shifting toward formats with stronger visibility, convenience and destination appeal.

Economic Conditions Still Shaping Market Sentiment

APS said the broader property market remains influenced by macroeconomic conditions, including slower domestic credit growth, higher operating costs and external geopolitical risks.

The report referenced Cambodia’s projected GDP growth of 5.5%, alongside foreign direct investment of around $5 billion, up 16% year-on-year. Those trends may help support medium-term confidence, particularly in sectors linked to manufacturing, infrastructure and urban expansion.

However, tighter financing conditions and more cautious sentiment mean buyers, tenants and investors are likely to remain selective through the remainder of the year.

If you are interested in learning more about Cambodia’s property market or for more information Telegram / WhatsApp +855 963 994 083