Cambodia Investment Review

Cambodia’s condominium market is entering a new phase of recovery and consolidation, with investors increasingly prioritising quality developments, central locations, and trusted developers, according to the Cambodia Condo Investment Guide 2026 by realestate.com.kh.

The latest data suggests a shift away from speculative buying toward more informed, end-user driven demand, as both local and international investors return to the market following a period of adjustment.

For more information, investment opportunities, or to speak directly with a property advisor: WhatsApp / Telegram: +855 963 994 083

A Market Shifting Toward Quality & Cautious Optimism

The report highlights a clear “flight to quality” across Cambodia’s property sector, with buyers now placing greater emphasis on project fundamentals, including developer reputation, pricing alignment, and long-term livability.

This shift reflects lessons learned from earlier market cycles, where speculative developments underperformed, leading investors to adopt a more cautious and selective approach.

At the same time, underlying confidence remains, supported by steady economic growth, urbanisation, and infrastructure development. Cambodia’s GDP is expected to remain above 5% through 2025 and 2026, driven by manufacturing, construction, tourism, and domestic consumption.

Developers are responding by improving product offerings, introducing more flexible payment structures, and focusing on lifestyle-oriented developments that align more closely with real buyer demand.

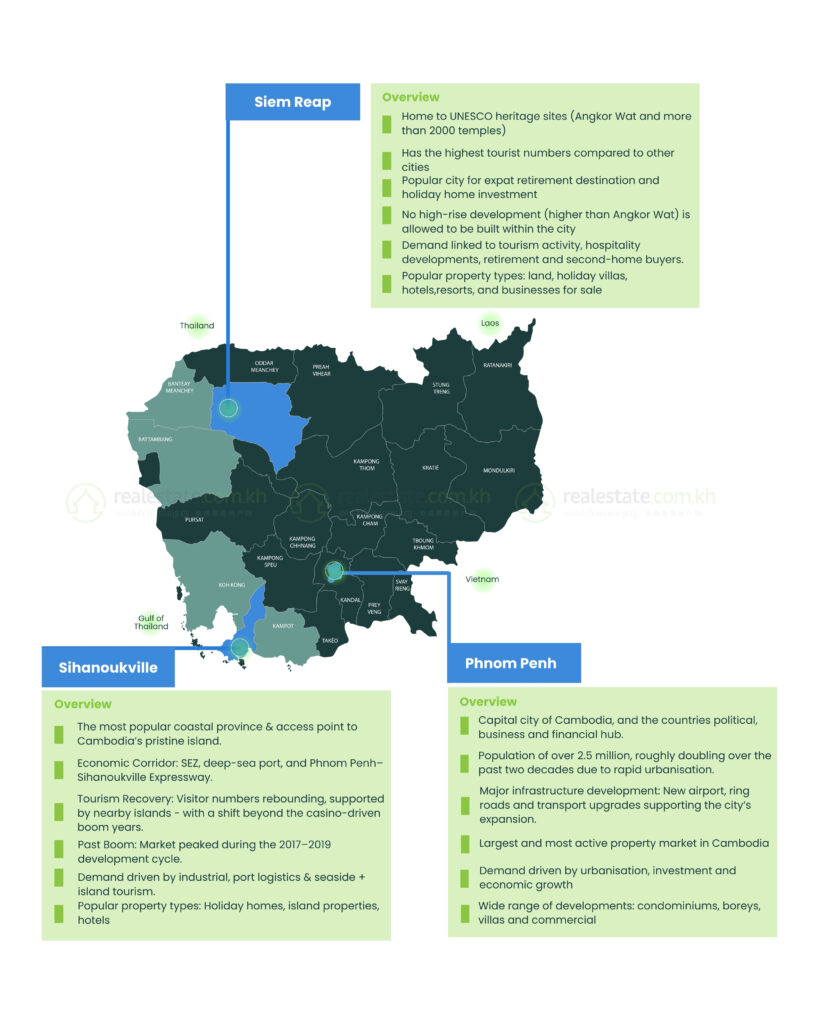

Phnom Penh Leads While New Markets Emerge

Phnom Penh continues to dominate Cambodia’s condominium market, accounting for over 70% of total purchases, with BKK1 remaining the most sought-after district for both investors and end-users.

The capital’s role as Cambodia’s political and financial centre, combined with ongoing infrastructure upgrades, continues to support its long-term appeal.

At the same time, emerging destinations such as Sihanoukville and Siem Reap are gaining traction.

Sihanoukville is showing signs of recovery following significant infrastructure investments, including the Phnom Penh–Sihanoukville Expressway and broader logistics development. Tourism recovery and renewed interest in coastal living are contributing to improved sentiment.

Siem Reap, while more constrained in large-scale condominium supply, is attracting niche investment focused on lifestyle and tourism-linked assets.

Foreign Buyers Dominate As Local Demand Strengthens

International investors remain a key driver of Cambodia’s condominium market, accounting for more than 60% of purchases, with notable activity from the United States, Europe, and regional markets.

However, domestic demand is steadily increasing, with Cambodian buyers representing a growing share of transactions. This trend is being driven by rising incomes, urban migration, and changing lifestyle preferences among younger professionals.

The increase in local participation is helping stabilise the market and shift it toward more sustainable, end-user driven growth.

Buyer preferences remain concentrated in smaller units, with one-bedroom apartments accounting for approximately 61% of purchases, reflecting affordability and strong rental demand.

Rental Market Remains a Key Support

The rental market continues to underpin investment activity, with one-bedroom units dominating demand at 72% and average rents reaching around $900 per month.

Demand is supported by a diverse mix of tenants, including Cambodian nationals and expatriates from across Asia, Europe, and North America, highlighting the increasingly international nature of Cambodia’s urban centres.

Well-located and well-managed projects continue to demonstrate the potential for stable rental income alongside long-term capital appreciation, particularly in central districts such as BKK1 and Tonle Bassac.

Supply pressures meet long-term opportunity

Cambodia’s total condominium supply reached approximately 64,000 units in 2025, raising questions around short-term absorption and market balance.

However, rather than a simple oversupply issue, the report suggests the market is undergoing a structural reset. Older, speculative projects are being filtered out, while newer developments are increasingly aligned with buyer expectations.

Several new project launches in early 2026 indicate that developers remain confident in the market’s long-term fundamentals, particularly as demand from both local buyers and international investors gradually strengthens.

As Cambodia continues to urbanise and its middle class expands, the condominium sector is expected to remain a key part of the country’s evolving real estate landscape.

Download the full 2026 report here.

For more information, investment opportunities, or to speak directly with a property advisor: WhatsApp / Telegram: +855 963 994 083