Cambodia Investment Review

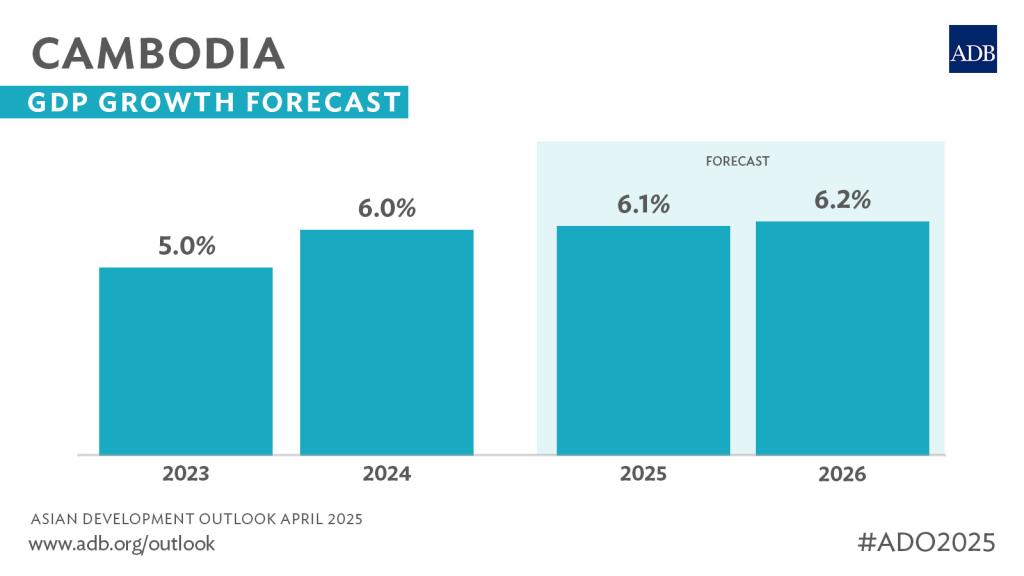

Cambodia’s economy grew by an estimated 6.0% in 2024, up from 5.0% in 2023, supported by a strong rebound in garment exports, sustained non-garment manufacturing, and a revival in tourism. However, challenges persist in the construction and real estate sectors, and inflation is projected to rise in 2025, tempering the otherwise positive outlook.

According to the Asian Development Bank’s Asian Development Outlook April 2025, while the economy is expected to continue expanding—reaching 6.1% growth in 2025 and 6.2% in 2026—maintaining momentum will require targeted investments in digital infrastructure and workforce development to address structural weaknesses and boost productivity.

Mixed Sectoral Performance in 2024

Industry was the key growth driver in 2024, expanding by 9.2% year-on-year. The garment sector surged with 23.5% export growth, while non-garment exports such as electrical components, vehicle accessories, and wooden goods grew at a slower 6.2%, compared to 20.7% the previous year. Construction activity saw a gradual recovery, but output remained below pre-pandemic levels due to weak domestic demand.

Read More: ADB Maintains Cambodia’s Economic Growth Forecast Amid Key Sector Rebounds

The services sector grew by an estimated 4.5%, largely on the back of tourism. International arrivals increased by 22.9% to 6.7 million, returning to pre-pandemic numbers. However, the majority arrived by land, indicating a shift toward more budget-conscious regional tourists. Real estate activity remained subdued amid a market correction.

Agriculture grew modestly at 0.9%, despite facing El Niño-related drought conditions until May. Crop production was supported by rising export demand and regional trade, with exports of cassava, rubber, and cashew nuts leading the gains. An improved freshwater fish catch also contributed to the sector’s performance.

Inflation Eases, But Set to Rise

Inflation averaged just 0.8% in 2024, down from 2.1% in 2023, due to lower fuel prices and stabilised food costs. However, inflationary pressures are building, with projections showing a rise to 3.7% in 2025 before moderating to 2.4% in 2026. The increase is attributed to a low-base effect and higher domestic demand, particularly for food.

The exchange rate remained stable, averaging KHR 4,071 per US dollar in 2024. While money supply (M2) expanded by 17.5%, credit to the private sector held steady at 3.9%, as rising nonperforming loans—especially in real estate—tempered bank lending.

Budget Deficit Widens, Debt Remains Manageable

Cambodia’s fiscal deficit reached $0.9 billion in 2024, or 1.9% of GDP, with both revenue and expenditure declining compared to 2023. Revenue dropped to $6.6 billion (14.5% of GDP) from $6.9 billion, reflecting tax incentives and lower taxable earnings. Spending decreased to $7.5 billion (16.4% of GDP), attributed to delayed budget execution.

Read More: ADB Inaugurates New Office in Cambodia with Deputy PM and ADB President

Public debt remained stable at 26.3% of GDP. Total debt stood at $11.9 billion, with external debt making up the bulk at 26.1% of GDP. The government issued $74.9 million in sovereign bonds to support infrastructure projects, raising domestic public debt to $115.1 million.

Outlook for 2025–2026: Opportunities and Constraints

Cambodia’s economic outlook remains largely positive, with real GDP growth forecast at 6.1% in 2025 and 6.2% in 2026. Industry will continue to lead expansion, with industrial output projected to grow by 9.3% each year, supported by both garment and non-garment exports. Foreign direct investment into manufacturing rose 56.7% in 2024, indicating sustained investor confidence.

The services sector is expected to grow by 4.4% annually, helped by rising tourist arrivals, particularly from Southeast Asia. However, recovery in the real estate market is likely to remain slow, partly due to reduced foreign investment and tighter credit conditions.

Agriculture is projected to grow by 1.0% in 2025 and 1.1% in 2026, bolstered by stronger trade links and foreign demand. Recent bilateral agreements with China and South Korea, along with participation in the Regional Comprehensive Economic Partnership (RCEP), are expected to support long-term growth in the sector.

Cambodia’s current account balance shifted from a 1.3% surplus in 2023 to a 0.2% deficit in 2024, as rising imports outpaced exports. The merchandise trade deficit widened to 9.9% of GDP, though services trade remained in surplus due to the tourism recovery. Foreign investment reached $4.4 billion in 2024, helping boost international reserves to $22.5 billion, covering nearly eight months of imports.

The government has set a higher budget deficit target of $1.5 billion (3.0% of GDP) for 2025, with planned revenue of $7.6 billion and spending of $9.1 billion. To support this, a new Revenue Mobilization Strategy for 2025–2028 was launched, aiming to modernize tax administration and enhance collection efficiency.

Digital Infrastructure and Productivity a Key Priority

ADB analysts emphasized that Cambodia’s past decade of growth has been investment-led, with limited gains in productivity. To sustain future growth and successfully graduate from Least Developed Country status by 2029, a shift toward productivity-led development is needed.

Digital technology is seen as a key enabler of this shift. By improving efficiency across agriculture, industry, and services, digital tools can create new economic opportunities while rejuvenating traditional sectors. For instance, precision agriculture, advanced manufacturing systems, and e-commerce platforms all offer high-potential gains.

However, gaps in digital infrastructure, skills, and regulatory frameworks remain barriers. Cambodia ranked 120th out of 193 countries in the UN’s 2024 e-Government Development Index, behind regional peers like Vietnam and the Philippines.

To address this, the government has initiated reforms and investments in digital public infrastructure, including digital ID systems (Khmer ID), broadband expansion, data center development, and cybersecurity. These efforts are complemented by policy frameworks such as the Digital Economy and Society Policy (2021–2035) and the Digital Government Policy (2022–2035).

Risks on the Horizon

Despite the promising trajectory, the ADB warns of downside risks. These include the potential for new trade barriers affecting Cambodia’s exports, further stress in the financial sector from rising nonperforming loans, and the impacts of extreme weather events on agriculture.

Nonetheless, with continued structural reforms and targeted investments—especially in digital technology and public infrastructure—Cambodia is well-positioned to maintain steady, inclusive growth in the years ahead.