Cambodia Investment Review

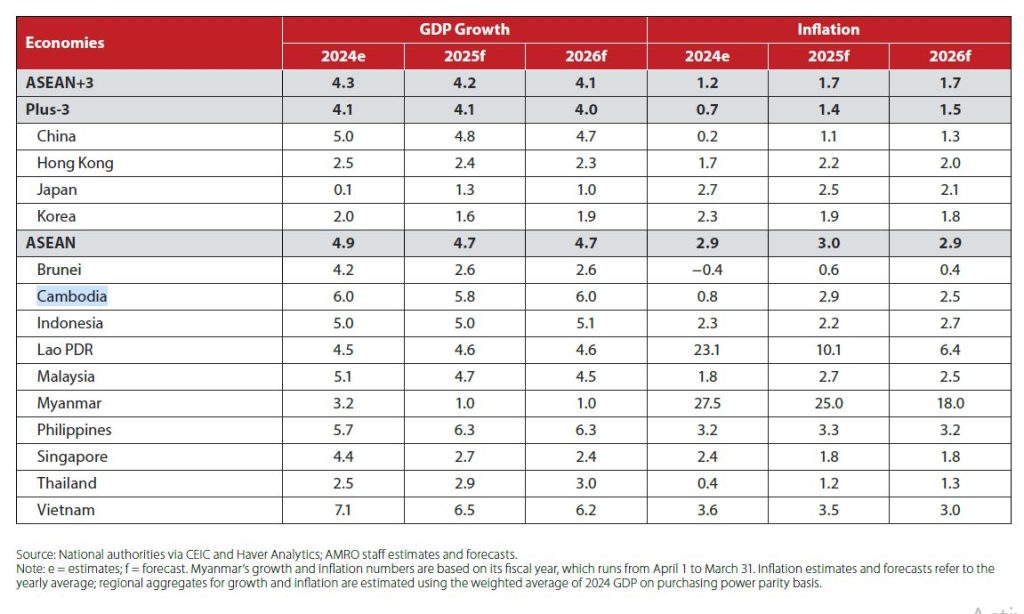

Cambodia’s economy grew by 6.0% in 2024, up from 5.0% in 2023, driven by a strong rebound in the garment sector and continued expansion in agriculture, according to the ASEAN+3 Regional Economic Outlook 2025. Looking ahead, the country’s GDP is projected to rise further to 6.4% in 2025. However, the overall recovery remains uneven, with services and real estate lagging, while financial sector risks are mounting due to rising nonperforming loans and subdued credit growth.

The report was released before new U.S. tariff measures under the Trump administration were announced, a development that may reshape Cambodia’s external trade dynamics going forward.

Read More: Opinion: US Tariffs – Cambodia’s Path To Resilience

Garment Sector Leads Growth, Services and Real Estate Trail

Cambodia’s garment exports rose 23.5% in 2024, benefiting from strong demand in the U.S. and EU markets. Agriculture also expanded, supported by multilateral trade agreements and rising investments in agri-food processing. These two sectors were the primary engines of growth in 2024.

In contrast, the services sector underperformed as the tourism recovery remained sluggish. Ticket sales for Angkor Wat reached only 51.7% of pre-pandemic levels. Meanwhile, the real estate sector continued to struggle due to persistent oversupply and weakened demand. Only 12 new residential projects were launched during the year, and mortgage loans declined by 5% year-on-year. The residential property price index also fell consistently since September 2023.

Inflation Eases, Currency Appreciates Slightly

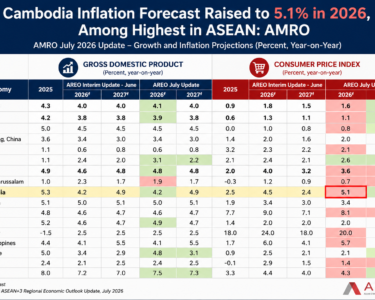

Inflation dropped significantly in 2024, with headline consumer price growth averaging just 0.8%—down from 2.1% in 2023. The decline was driven by lower energy and food prices. Core inflation also remained low at 0.9%, reflecting weak domestic demand. Inflation is expected to remain subdued in 2025, providing some monetary policy flexibility.

The Cambodian riel appreciated marginally to an average exchange rate of KHR 4,071 per USD in 2024, following seasonal patterns. International reserves increased to USD 22.5 billion, equivalent to 9.4 months of imports, suggesting external sector stability despite emerging challenges.

Current Account Deficit Widens

Cambodia’s current account balance recorded a slight deficit of 0.1% of GDP in 2024, as imports grew 17.6%—outpacing export growth of 13.6%. The trade deficit based on customs data widened to 7.8% of GDP. However, resilience in FDI inflows, at 8.7% of GDP during the first three quarters, helped mitigate pressure on external accounts. The 2025 outlook points to further narrowing of the current account deficit if export conditions remain stable.

Financial Sector Under Pressure

Credit growth decelerated sharply, with domestic credit increasing just 2.2% in 2024 and private sector credit up only 3.1%. Nonperforming loans climbed to 7.3% by December, prompting banks to adopt more cautious lending strategies. Return on assets fell to 0.2%, underscoring profitability concerns.

Although the banking system remains robust—with a capital adequacy ratio above 20% and a liquidity coverage ratio above 160%—rising credit risks and weak loan demand, particularly in real estate, pose downside risks to financial stability.

Read More: Two Leading Cambodian Banks Show Mixed Results During the Banking Sector Slowdown of 2023

Fiscal Deficit Narrows on Spending Cuts

The fiscal deficit improved to 3.6% of GDP in 2024 from 5.3% in 2023, driven by expenditure rationalization. Tax revenue grew modestly by 2.1% year-on-year but reached only 86.9% of the government’s target, due in part to tax incentives and weak economic activity. Public debt declined slightly to 26.1% of GDP, supported by stronger nominal GDP and lower primary deficits.

2025 Outlook: Moderate Growth Amid External Uncertainty

For 2025, Cambodia’s real GDP is forecast to grow by 6.4%, supported by continued recovery in manufacturing and agriculture, along with gradual improvements in services. However, the report cautions that downside risks remain prominent.

Cambodia is vulnerable to global economic shifts—particularly slower growth in China and potential trade policy adjustments by the U.S. and EU. With more than half of Cambodia’s goods exports destined for these two markets, future changes to preferential trade access, such as the EU’s EBA scheme, could weigh on export performance.

In addition, further deterioration in loan quality, especially among smaller banks and real estate developers, could amplify financial sector risks.

Cambodia’s economy showed solid recovery momentum in 2024 and is poised for moderate growth in 2025. Yet, key sectors such as services and real estate remain weak, and credit quality issues are emerging. While macroeconomic stability has improved—highlighted by low inflation, stable reserves, and a narrowing fiscal deficit—continued vigilance is needed to manage financial sector vulnerabilities and navigate rising external uncertainties.