Cambodia Investment Review

Cambodia’s banking sector generated approximately $1 billion in total net profit in 2025, with earnings heavily concentrated among a small group of leading institutions, according to newly compiled financial data by the National Bank of Cambodia report.

The data highlights a clear trend of profit concentration, with the country’s four largest banks — Advanced Bank of Asia (ABA), ACLEDA Bank, KB Prasac Bank, and Canadia Bank — collectively accounting for more than $750 million in net profit. This represents roughly three-quarters of total earnings across the commercial banking sector.

The sector remains highly competitive, with 59 commercial banks operating in Cambodia in 2025, further underscoring the concentration of profitability among a relatively small group of top-tier institutions.

This performance comes amid a more uncertain global and regional environment, with Cambodia’s economy projected to grow at around 5% in 2025, reflecting external pressures and ongoing regional dynamics.

Top-tier banks dominate sector profitability

The top four banks delivered the strongest results in 2025:

• ABA Bank: ~1.51 trillion KHR (~$377M)

• ACLEDA Bank: ~741 billion KHR (~$180M)

• KB Prasac Bank: ~430 billion KHR (~$105M)

• Canadia Bank: ~394 billion KHR (~$95M)

Together, these four banks generated over 3 trillion riel in profit, reinforcing their dominant position within Cambodia’s financial system. Their performance reflects strong deposit bases, nationwide branch networks, diversified lending portfolios, and continued investment in digital banking infrastructure.

These institutions have been better positioned to maintain profitability at scale, even as credit growth moderates and provisioning costs increase across the sector.

Loss-making banks highlight uneven performance

While leading banks recorded strong profits, several institutions reported losses in 2025, underscoring the increasingly challenging operating environment:

• Hattha Bank: ~-371 billion KHR (~-$90M)

• Taiwan Cooperative Bank (Phnom Penh Branch): ~-77 billion KHR (~-$19M)

• HH Bank (Cambodia): ~-55 billion KHR (~-$13M)

• CCU Commercial Bank: ~-43 billion KHR (~-$10.5M)

These losses reflect a combination of rising provisions linked to non-performing loans, margin compression in a highly competitive market, and slower credit growth, particularly in sectors such as real estate and construction.

The divergence between top-performing and loss-making banks highlights a widening gap within Cambodia’s banking sector, as larger institutions continue to scale while smaller or more exposed banks face increasing financial pressure.

Sector remains resilient despite rising risks

Despite these disparities, the National Bank of Cambodia (NBC) noted that the overall banking system remains resilient, supported by strong capital adequacy and liquidity levels above regulatory minimums.

Total banking system assets increased by 8.2% in 2025, while customer loans grew by 5.4% and deposits rose by 12.4%, reflecting continued public and investor confidence in the sector.

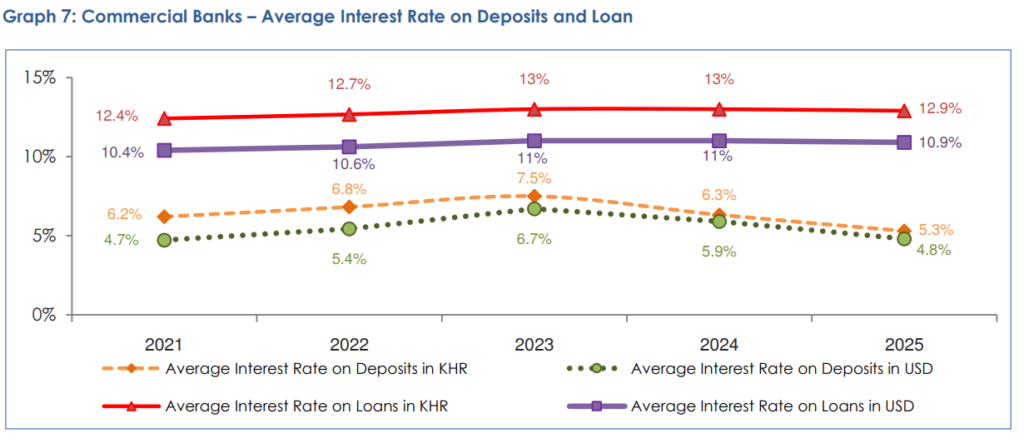

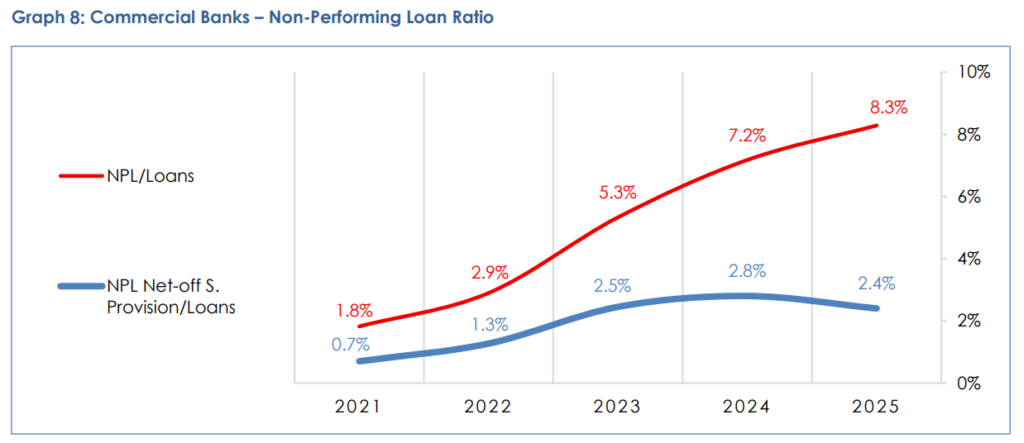

At the same time, asset quality pressures have emerged, with the non-performing loan (NPL) ratio rising to 8.6%, although the net NPL ratio remained contained at 2.4%, supported by a provisioning coverage ratio of 71.2%.

The NBC has also continued to strengthen supervision, enhance reporting standards, and promote digital payment systems and sustainable finance initiatives, positioning the sector for longer-term stability and growth.

Sector enters more mature phase

The concentration of profits among leading banks comes as Cambodia’s financial sector transitions into a more mature phase following a decade of rapid expansion.

While deposit growth has remained relatively stable, lending activity has slowed, reflecting tighter credit conditions and a shift toward more sustainable growth. At the same time, the rapid adoption of digital payments, including QR-based systems, continues to reshape the competitive landscape.

Looking ahead, profitability is expected to remain concentrated among a handful of top-tier institutions, with banks needing to balance growth, risk management, and operational efficiency in an increasingly disciplined environment.

The performance of ABA, ACLEDA, KB Prasac, and Canadia Bank in 2025 underscores their role as key drivers of sector profitability, even as the broader market adjusts to a more complex and competitive landscape.