Kim Sopheakrakboth

The rise of low-cost aviation carriers (LCC) has redrawn the map of global travel. For Cambodia — while rebuilding its visitor economy — this phenomenon is not just an opportunity. It is a defining moment.

The age of budget aviation has quietly transformed the way the world moves.

Across Southeast Asia, carriers like AirAsia, Scoot, Vietjet, and Lion Air have turned a leisure trip to a distant country from a luxury into an impulse decision — the kind of decision made on a smartphone at midnight.

Fares that once required months of saving are now clear on a lunch-break chat. And wherever these airlines land, tourist economies usually follow.

For Cambodia, this revolution could not arrive at a more pivotal juncture. The tourism sector — one of its most significant economic engines — is still finding its footing after years of pandemic disruption.

Visitor numbers, while recovering, have not yet reached the level recorded in 2019 because the underlying infrastructure of accessibility that bring travellers to these shores in the first place remains a work in progress.

LLC and the Democratisatin of Travel

What budget airlines have done, fundamentally, is obliterate the perceived distance between the destination and its source markets.

The cost has long been one of the major deterrents for mid-market and budget-conscious travellers, to whom Cambodia has always been an appealing destination in the abstract but a relatively expensive and inaccessible one in practice. Low-cost carriers have the potential to ease that friction.

The evidence from comparable markets is compelling. When VietJet — Vietnam’s first and most successful privately-owned low-cost carrier — launched its maiden flight in December 2011, it triggered a structural shift in regional aviation.

Vietnam’s international arrivals grew from 5.9 million in 2011 to 12.9 million in 2017 — more than doubling the pre-Vietjet arrival within six years. According to the Civil Aviation Administration of Vietnam, annual passenger growth averaged 14 percent every year between 2010 and 2017, one of the fastest rates anywhere in the world during that period. By 2019, VietJet air had captured 42.6 percent of Vietnam’s total flight volume.

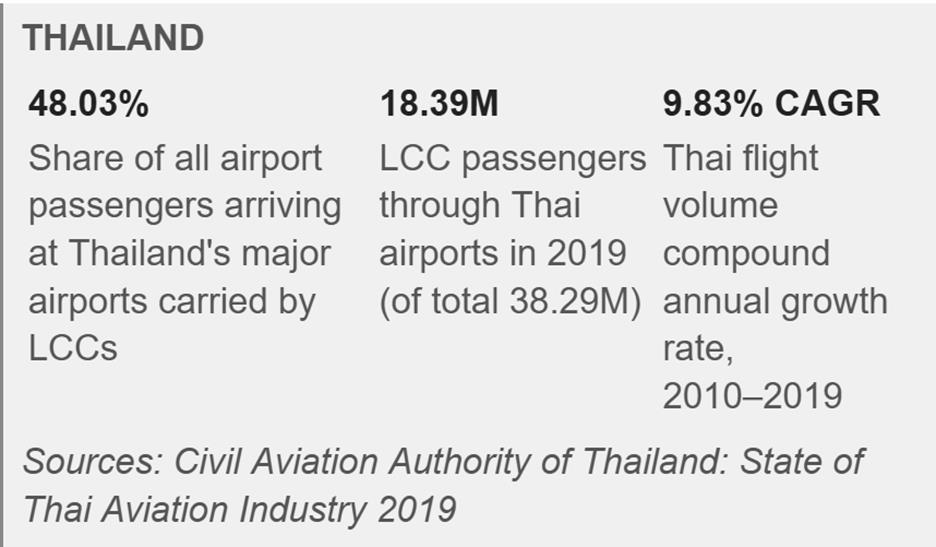

Thailand’s story is equally instructive, and perhaps more relevant as a long-run model.

The country’s transformation into the most-visited destination in Southeast Asia and ability to retain the status is inseparable from the rise of LCC.

By 2019, low-cost carriers accounted for 48 percent of all air passengers across Thailand’s six major airports — 18 million of 38 million total travellers — with Bangkok’s Don Mueang airport repurposed almost entirely as an LCC hub for regional and international routes.

Thai air transport posted a compound annual growth rate of 9.83 percent between 2010 and 2019, driven in no small part by the frequency and affordability that budget carriers brought to routes from China, Japan, South Korea, India and ASEAN countries.

“Every new low-cost route to Phnom Penh and Siem Reap is, in effect, a new market unlocked — a new population of travellers for whom Cambodia just became very accessible.”

Current Cambodian Context

While LCCs have captured a significant share of seat capacity in Thailand and Vietnam, Cambodia’s LCCs penetration remains at 21 percent due to operational cost constraints and a softer demand.

Optimistically speaking, Cambodia’s situation has several features that could make budget airline connectivity especially consequential.

First, the infrastructure is already there. The country’s two primary gateways — Techo International Airport and Siem Reap Angkor International Airport — both have tremendous capacity with facilities that are ready to serve the volume that low-cost carriers could bring: spacious and high-throughput. It is, in a sense, infrastructure built in anticipation of an aviation uninterrupted growth.

Second, Cambodia’s tourism product is still disproportionately reliant on first-time visitors despite product diversification efforts.

Unlike Thailand or Bali, which generate a significant share of revenue from repeat travellers, Cambodia tends to be a ‘bucket list’ destination — Angkor Wat. That means the top of the funnel matters enormously.

Budget airlines are, above all, funnel-wideners and barrier dismantlers. They lowered the barrier for the first-time visitors who then discover that Cambodia has far more to offer than a single visit can accommodate.

Third, and perhaps most urgently, Cambodia is competing in an increasingly crowded regional market. Vietnam has aggressively positioned itself as a multi-city, year-round destination.

Thailand has an unmatched marketing infrastructure. Indonesia’s Bali remains a gravitational centre for global leisure travel.

For Cambodia to grow its share, price accessibility cannot be an afterthought — it must be one of the strategic priorities. A flight to Phnom Penh that costs 30-50 percent more than a comparable flight to Ho Chi Minh or Bangkok is a flight that many travellers will quietly reconsider.

Benefits Beyond the Arrival Gate

The benefits of budget airline connectivity extend well past the arrival gate. Lower airfares free up more budget to spend within the destination that could lead to longer average stays because travellers who saved on their flight are now able to extend their trip by a few days.

They stay in hotels that feed into local supply chains. They eat at family-run restaurants rather than resort buffets. The distributional effect on local informal economies — particularly in secondary destinations like Kampot, Battambang and the islands of Koh Rong — can be profound.

There is also a powerful case to be made for the human dimension of this connectivity. Tourism is, at its core, an act of encounter.

Every budget traveller who lands in Phnom Penh and spends a week navigating Cambodian streets, history and hospitality goes home as an informal ambassador.

In an era where Cambodia’s global narrative is too often shaped by geopolitical coverage, the human-centric nature of tourism — genuine, personal encounter — is undoubtedly invaluable to Cambodia’s tourism recovery.

What’s Next for Cambodia

Connectivity alone is not sufficient. The establishment of more budget flight routes must be accompanied by improvements of the whole visitor experience — visa application, airport & immigration process, safety, connectivity between tourist sites, digital infrastructure, and quality of hospitality services — all determine whether a first visit becomes a return visit or a cautionary tale shared with friends back home.

Budget travellers are not low-expectation travellers. They are value-conscious ones. This distinction matters.

The Ministry of Tourism, the State Secretariat of Civil Aviation, Cambodia Airport and tourism operators have a shared interest in making this work.

Incentive structures for new LCC routes such as reduced landing fees and ground handling costs, along with co-marketing arrangements, have proven effective in comparable regional markets and deserve serious policy attention.

The Thai model, in which government bodies actively incentivise route development through fee reductions and parking‑charge discounts for new routes and new airlines, offers a useful template. The policy is formally carrier‑neutral (not LCC‑specific), though in practice LCCs have been the primary beneficiaries.

There is also a case for diversifying the source markets that budget connectivity opens up.

Cambodia’s visitor base is heavily weighted toward China and Vietnam. Budget airline routes to India — the world’s fastest-growing outbound travel market — South Korea and Japan, where Cambodia has already developed a matured market presence, represent genuine growth frontiers.

These routes will not materialise on their own. They require proactive, upfront and sustained investment.

This does not mean that Full Service Carriers (FSC) do not have a place in Cambodia tourism recovery strategy. FSC plays a critical role in connecting travellers who are less price-sensitive especially from the long-haul market into major regional-hubs.

They are complementary channels serving complementary market segments. The recent agreements between the Cambodia Tourism Board with Singapore Airlines and AirAsia Cambodia signal that the industry truly values the importance of each carrier type. Connectivity is not a byproduct of tourism recovery — it is a precondition for it.

The infrastructure is ready. The gates are built. The rest depends on us.

The views and opinions expressed are those of the author and do not reflect the official policy and the position of the organization he’s associated with.

Kim Sopheakrakboth is senior market researcher at Cambodia Tourism Board. He holds a masters degree in public policy with a specialization in economics and development from the Lee Kuan Yew School of Public Policy at the National University of Singapore. His work focuses on the experiential economy — particularly how events, tourism and cultural assets can be leveraged to drive local spending and sustainable economic development.