Raymond Sia

ASEAN expatriate employees drawing their remunerations in US Dollar (“Dollar”) or pegged against the Dollar in the past months would have felt different emotions; depending on their domiciled working country where they are based.

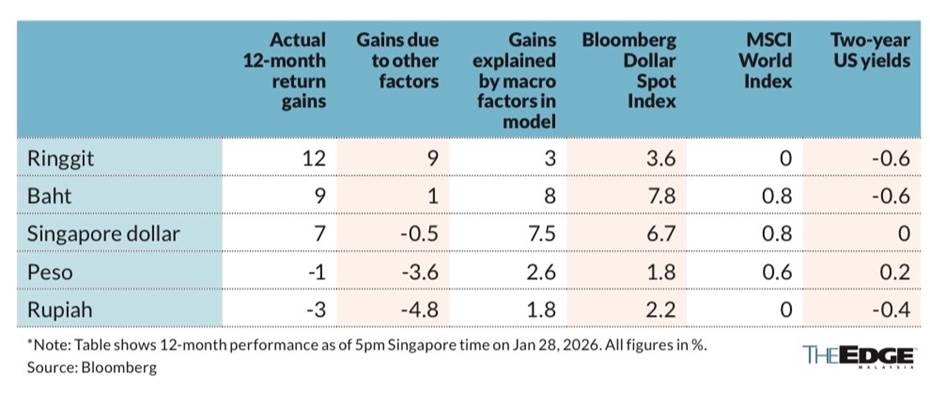

Based on the table above; as at 28 January 2026, employees from Malaysia, Thailand and Singapore would have experienced a “pay cut” of 12%, 9% and 7% respectively the past 12 months while Indonesian and Philippine expatriate employees would have seen a modest “pay hike” of 3% and 1% respectively in the same corresponding period.

- Attractions or Distractions?

Many other foreign currencies have been outperforming the Dollar in 2025 (obviously) and the key question is whether one should start moving-away from Dollar savings and converting the Dollar income to other currencies.

Yield or anticipated or actual returns play an important part to this question.

The forecast for the Dollar is predicated on a number of factors which includes interest rate directions (for Dollar & other currencies) and perceived state of the US economy vs other global economies.

| Actual | Forecast | |||

| As at 14 February 2026 | March 2026 | June 2026 | December 2026 | |

| Interest Rate | ||||

| US Federal Reserve | 3.5% – 3.75% | 3.50% – 3.75% | 3.25% – 3.50% | 3.00% – 3.25% |

| Bank of England | 3.75% | 3.50% | 3.50% | 3.25% |

| Bank Negara Malaysia | 2.75% | 2.75% | 2.75% | 2.75% |

| Foreign Exchange | ||||

| GBP / USD | 1.35 | 1.34 | 1.31 | 1.30 |

| USD / MYR | 3.95 | 4.00 | 4.10 | 4.08 |

Interest Rate & Foreign Exchange forecast by the Author

We are mindful that the longer-term interest rate trend in both developed and emerging markets are expected to be on a downward trend; but any surprises in economic data (namely inflation and employment data) may cause volatility in interest rates.

The recent January 2026 Federal Reserve (“Fed”) Open Market Committee’s meeting minutes revealed many Fed officials were surprisingly wary of cutting interest rates, with several even suggesting the central bank may need to raise rates if inflation remains stubbornly high.

We have seen Reserve Bank of Australia (“RBA”) raising interest rates by 0.25% on 3 February 2026 due to resurgence in inflation, becoming the first major central bank to go from rate cuts to rate hikes following the post-COVID inflation spike. RBA is expected to have another interest rate hike if inflation is not abating.

Will we have more of such upside interest rate surprises in 2026?

- Relevant or Redundant?

There are nations which have congregated to form an alliance to reduce Dollar dependency i.e. BRICS or an alliance of (initially) five major emerging economies: Brazil, Russia, India, China, and South Africa which is working to also promote the usage of local-currency trade and the development of a potential new currency to replace the Dollar.

Geopolitical resistance further complicates any efforts to make the Dollar less relevant.

U.S. President Donald Trump has explicitly opposed BRICS’ financial independence efforts, warning that any attempt to bypass the Dollar would lead to a 100% tariff on any U.S. bound products from BRICS-nation. This threat of economic retaliation and sanctions deters many nations from shifting too quickly away from the Dollar, reinforcing its hold on global trade.

Based on recent financial reports, the Dollar continues to anchor its relevance in the financial realm with 59% of Foreign Exchange (“FX”) reserves held by central banks, 89% of FX trading volume and 80% of global payments & trade finance; all denominated in the Dollar. (Source: SWIFT RMB Tracker Report and BCA Research in January 2026)

Dollar may have loss some of its luster; especially in the last 12 months but certainly not its relevance.

- Potential or Pariah?

Is this the “beginning of the end” of the Dollar; with more capitulation in-store? Or is the worse over for the Dollar?

Currency traders the past months have taken more positions in shorting the Dollar or positioning for further Dollar weakness due to the uncertainty surrounding interest rate directions and economic data from inflation to job /unemployment data. The Fed itself is adding to the uncertainty with a new Fed Chairman starting in June 2026. It is a foregone conclusion that market perception is leaning towards a more dovish Fed moving forward; which will weigh on the Dollar and its real yield.

At the time of writing this article, the Dollar continue to trade sideways (vs many ASEAN currencies) with more downside bias unless inflation proves stickier than expected or a sudden geo-political shock occurs (think Iran & Middle East).

There are certainly more headwinds for the Dollar in 2026. Upside potentials are limited but the Dollar is certainly not an outcast.

Raymond Sia currently serves as the Managing Director of Canadia Investment Holding Plc and Board Director for Canadia Bank and Credit Bureau Cambodia.

Raymond is also the author of the “Right Angle – The Collection Volume One” which is now available for sale. The views expressed above are strictly the author’s personal opinion and do not represent the organisations & institutions he is attached with or represents.