Cambodia Investment Review

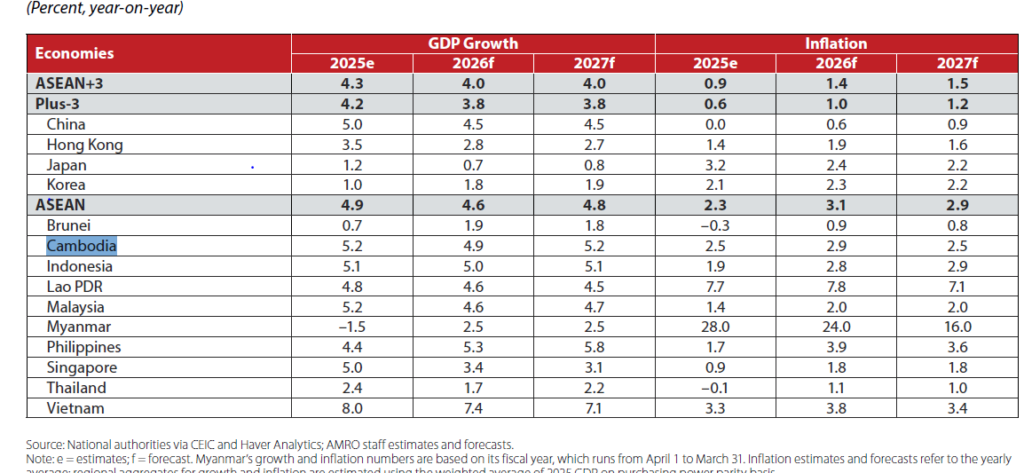

Cambodia’s economy is forecast to grow 4.9 percent in 2026, with inflation rising to 2.9 percent, according to the latest outlook from ASEAN+3 Macroeconomic Research Office, although the projections are increasingly overshadowed by escalating geopolitical risks linked to the Middle East conflict and global energy supply disruptions.

The figures, published in AMRO’s ASEAN+3 Regional Economic Outlook (AREO) 2026 on April 6, suggest Cambodia will maintain steady growth, before expanding further to 5.2 percent in 2027, with inflation easing back to 2.5 percent.

However, the report itself makes clear that the regional outlook has shifted, with risks now tilted firmly to the downside due to the ongoing conflict in the Middle East—raising questions over whether baseline forecasts, including Cambodia’s, were effectively set before the full impact of the Iran-linked escalation was reflected in global markets.

Cambodia outlook remains stable on paper

AMRO’s projections position Cambodia among ASEAN’s more resilient economies, with growth holding near 5 percent despite global uncertainty.

The Kingdom’s inflation trajectory also remains relatively contained compared to some regional peers, suggesting manageable domestic price pressures under current assumptions.

Across ASEAN, growth is projected at 4.6 percent in 2026 and 4.8 percent in 2027, while the broader ASEAN+3 region is expected to expand at 4.0 percent over the same period, following a stronger-than-expected 4.3 percent expansion in 2025.

This regional resilience has been supported by firm domestic demand, investment flows, and exports—particularly in sectors linked to technology and semiconductors.

For Cambodia, continued integration into regional supply chains and steady domestic consumption are expected to underpin growth in the near term.

Middle East conflict shifts risk outlook

Despite these relatively stable baseline projections, AMRO warned that the balance of risks has shifted materially to the downside due to geopolitical developments.

The report highlights that the impact of the Middle East conflict—particularly if prolonged—could extend beyond energy markets into broader economic channels including logistics, food prices, tourism, and remittances.

For Cambodia, which remains reliant on imported fuel and energy inputs, higher global oil prices could quickly translate into rising transport and production costs.

This creates potential second-round effects across key sectors such as manufacturing, construction, and services, while also putting upward pressure on inflation beyond the projected 2.9 percent for 2026.

The timing of the report suggests that while the forecasts reflect improving regional fundamentals, they may not fully capture the most recent escalation in geopolitical tensions and its implications for energy markets.

Structural resilience offers partial buffer

AMRO notes that the ASEAN+3 region is better positioned than in previous crises to absorb external shocks, citing improvements in energy efficiency, lower inflation starting points, and stronger policy frameworks.

Over the past two decades, the region has also become more internally integrated, with a growing share of trade and demand generated within ASEAN+3 rather than from external markets.

This structural shift provides some insulation for economies like Cambodia, particularly as intra-regional trade and investment continue to deepen.

However, the report cautions that external shocks—especially those linked to energy—remain a key vulnerability for smaller, open economies.

Policy response seen as critical

AMRO emphasizes that maintaining policy flexibility will be essential in managing the evolving risk environment.

Central banks are encouraged to ensure financial stability and respond decisively if supply-side shocks lead to sustained inflation, while governments are advised to focus on targeted support for vulnerable groups rather than broad-based fiscal measures.

For Cambodia, this could involve balancing support for households facing rising living costs with the need to maintain fiscal discipline and macroeconomic stability.

Outlook increasingly dependent on global developments

While Cambodia’s projected recovery to 5.2 percent growth by 2027 reflects confidence in its medium-term fundamentals, the near-term outlook is becoming more uncertain.

The trajectory of the Middle East conflict—and its impact on global energy prices—will be a key determinant of whether current forecasts hold.

AMRO concludes that although the region entered 2026 from a position of strength, the evolving global environment could test that resilience.

For Cambodia, the outlook remains positive on paper, but increasingly contingent on external factors that are largely beyond domestic control.