Cambodia Investment Review

Cambodia’s small business credit market showed further signs of strain in the final quarter of 2025, with rising non-performing loans (NPLs), declining credit demand, and a continued contraction in the number of active loan accounts, according to the latest Small Business Credit Index released by Credit Bureau Cambodia (CBC).

The data points to a more cautious lending environment for micro, small and medium-sized enterprises (MSMEs), as both borrowers and lenders adjust to softer demand conditions and elevated credit risk across key sectors of the economy.

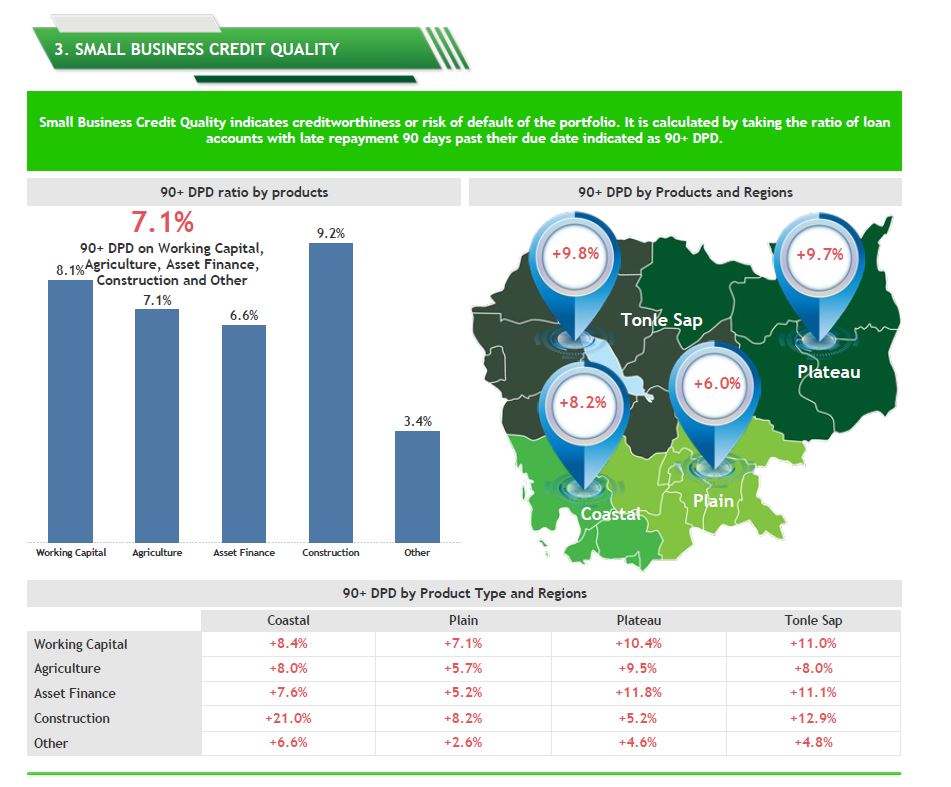

Credit quality weakens across major loan categories

The overall NPL ratio for small business loans rose to 7.1 percent in Q4 2025, measured by loan accounts with repayments overdue by more than 90 days. The increase reflects mounting repayment pressure across Cambodia’s core MSME lending segments.

Construction loans recorded the highest level of stress, with a 90+ days past due ratio of 9.2 percent. Working capital loans followed at 8.1 percent, while agriculture loans reached 7.1 percent. Asset finance loans performed comparatively better, with an NPL ratio of 6.6 percent, while the “other” loan category recorded the lowest delinquency level at 3.4 percent.

Across regions, elevated delinquency ratios were observed nationwide, indicating that repayment challenges are becoming more widespread rather than concentrated in specific provinces. Construction-related loans showed particularly high increases in overdue repayments in the Coastal and Tonle Sap regions.

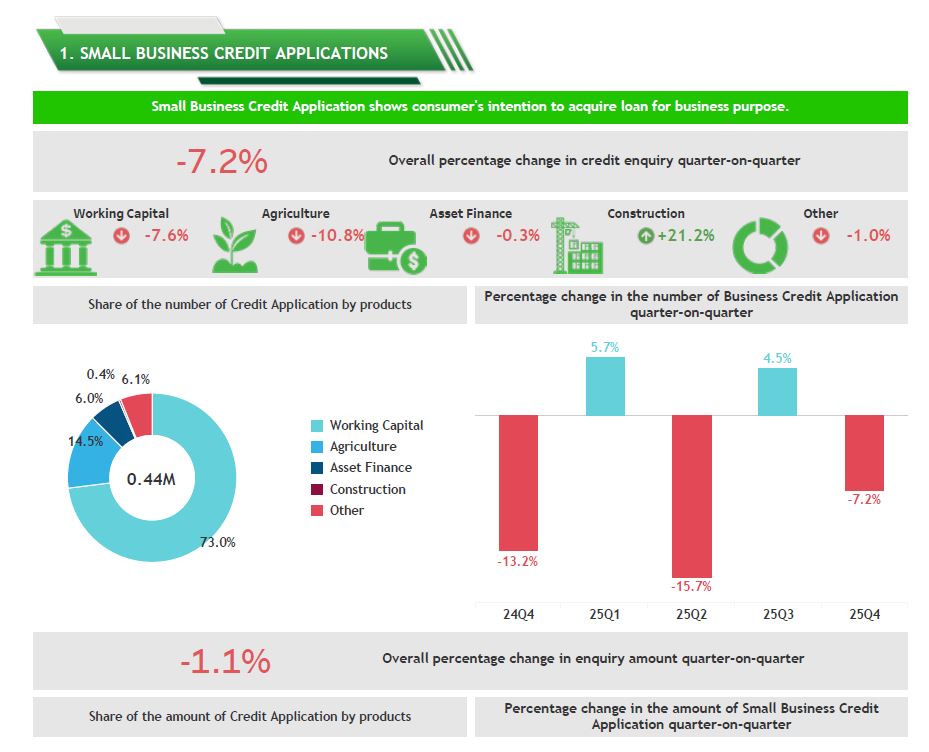

Credit demand declines as businesses turn cautious

The rise in credit stress coincided with a slowdown in new borrowing activity. The number of small business credit applications declined by 7.2 percent quarter-on-quarter, extending a volatile trend seen throughout 2025.

Changes in application volumes varied by loan type:

• Working capital applications declined by 7.6 percent and continued to account for roughly 73 percent of total credit demand

• Agriculture-related applications fell by 10.8 percent, reflecting pressure on rural and agribusiness operators

• Asset finance applications remained broadly stable, slipping by just 0.3 percent

• Construction loan applications rose by 21.2 percent, despite the segment recording the weakest credit quality indicators

In value terms, the total amount of credit applied for declined by 1.1 percent compared to the previous quarter, pointing to smaller loan sizes and more conservative borrowing behaviour among MSMEs.

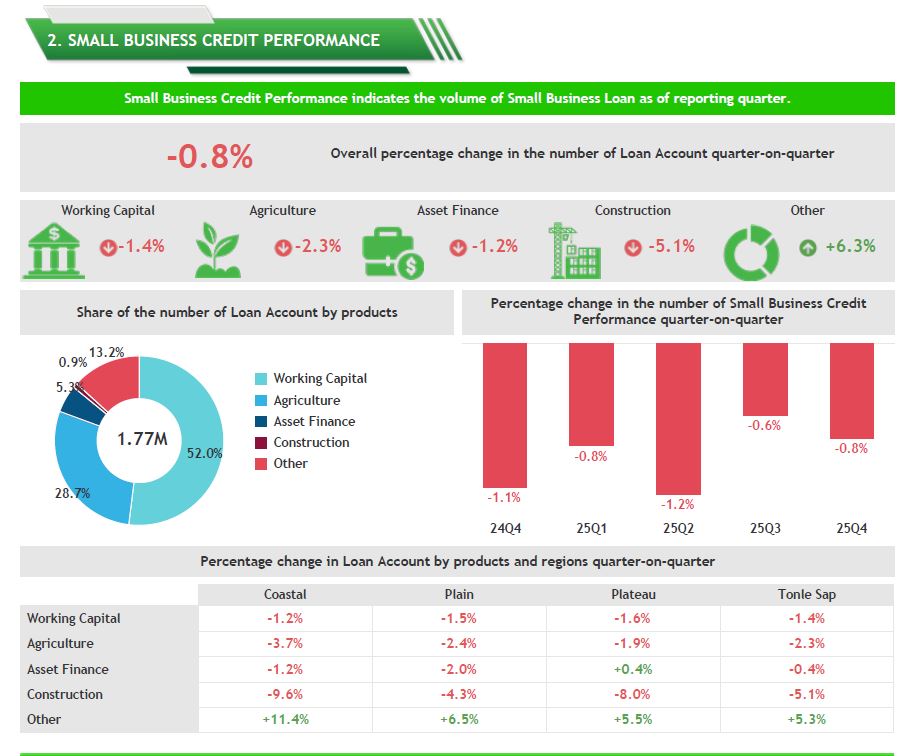

Loan accounts fall, while outstanding balances rise

The slowdown in credit demand translated into a further decline in the number of active loan accounts. The total number of small business loan accounts fell by 0.8 percent in Q4 2025, marking the fifth consecutive quarterly contraction.

By loan type:

• Construction loan accounts fell by 5.1 percent, reversing earlier gains

• Agriculture loan accounts declined by 2.3 percent

• Working capital loan accounts decreased by 1.4 percent

• Asset finance loan accounts slipped by 1.2 percent

• The “other” loan category recorded growth of 6.3 percent

Despite fewer loan accounts, outstanding loan balances continued to rise. Total small business loan balances increased by 2.6 percent quarter-on-quarter to approximately $37.12 billion.

Working capital loans accounted for 65.1 percent of outstanding balances, followed by agriculture at 15.4 percent and asset finance at 10.3 percent. Regionally, loan balances grew most strongly in the Coastal and Plain regions, while growth in the Plateau and Tonle Sap regions was more modest.

Outlook: selective lending likely to persist

Overall, the Q4 2025 Small Business Credit Index suggests a market in adjustment rather than outright contraction. Credit continues to expand in value, but is increasingly concentrated among fewer borrowers and larger exposures.

For lenders, the data highlights the importance of tighter risk management amid rising delinquency levels. For small businesses, particularly those in agriculture and construction, access to new credit may remain constrained until repayment performance stabilises and confidence in the operating environment improves as Cambodia moves into 2026.