Cambodia Investment Review

Cambodia’s economy demonstrated moderate growth in 2023, supported by a robust recovery in tourism and increased domestic consumption, according to the ASEAN+3 Regional Economic Outlook 2024 by the AMRO ASEAN+3 Macroeconomic Research Office (AMRO). However, the economic landscape does come with challenges, particularly in the real estate and financial sectors, and is highly vulnerable to global price fluctuations.

Growth Driven by Tourism and Domestic Consumption

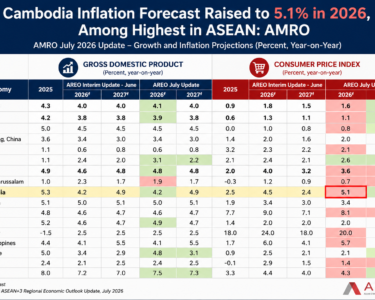

The nation’s GDP growth is estimated at 5.3 percent for 2023, a slight increase from 5.2 percent in 2022. This growth was primarily driven by improvements in the services sector, fueled by the resurgence in tourism and pent-up domestic consumption. The non-garment manufacturing sector also maintained high growth throughout the year. In contrast, the garment sector faced decelerated growth due to weak demand from the US and EU markets.

Inflation trends in 2023 showed significant moderation due to declining global oil and food prices. Consumer price inflation eased to an average of 1.2 percent in the first half of the year, largely due to a 6.3 percent reduction in energy prices. However, inflation rates began to rise from July 2023, influenced by the base effect from the previous year and tightening global rice supplies. By the end of the year, inflation had decreased to 2.1 percent, down from 5.3 percent in 2022.

Cambodia’s economy remains highly vulnerable to global price fluctuations, particularly spikes in oil and food prices triggered by geopolitical tensions or climatic anomalies such as El Niño. These factors can lead to heightened inflationary pressures, posing a significant risk to economic stability.

Real Estate Sector Challenges

Domestically, the real estate sector presents a major vulnerability. Despite its rapid growth, the sector is plagued by unregulated shadow banking activities that could potentially destabilize the financial system and, by extension, the broader economy.

The oversupply in the real estate market, resulting from a construction boom and increased foreign investments during 2018–2019, has led to liquidity problems for developers. In response, the government implemented support measures in April 2023, including tax payment postponements and exemptions for Borey developers and home buyers.

Credit expansion slowed, with the banking sector seeing a rise in the nonperforming loan ratio. Credit growth moderated from 18.2 percent in 2022 to an average of 13.4 percent from January to November 2023, driven mainly by lending in the real estate and wholesale and retail trade sectors. Nonperforming loans increased to 5.4 percent of bank loans by November 2023 from 3.1 percent in December 2022. Despite this, the banking sector remained sound, with a capital adequacy ratio exceeding 20 percent and a liquidity coverage ratio of 168 percent in November 2023.

Financial Sector Vulnerabilities

The financial sector is increasingly susceptible to liquidity crises due to its growing reliance on short-term external debt and non-resident bank deposits. These conditions could lead to sudden reversals of capital, threatening financial stability and economic security. The fiscal deficit widened to an estimated 6.9 percent of GDP in 2023, driven by reduced revenue collection and increased fiscal stimulus.

The government expanded the cash transfer program to include “near-poor” households and flood-hit communities, increased civil service wages, and invested in digital and green infrastructure projects. The fiscal deficit is expected to decline as fiscal consolidation plans take effect, though it will remain higher than pre-pandemic levels due to the integration of the COVID-19 cash transfer program into a permanent “Family Package” program for vulnerable households.

Several external risks could derail Cambodia’s economic recovery. These include potential economic slowdowns in China, the US, and the EU, spikes in global oil prices due to geopolitical tensions, and surges in global food prices triggered by severe El Niño conditions. Domestically, prolonged weakness in the real estate sector could pressure the financial sector, particularly through unregulated shadow banking activities.