Cambodia Investment Review

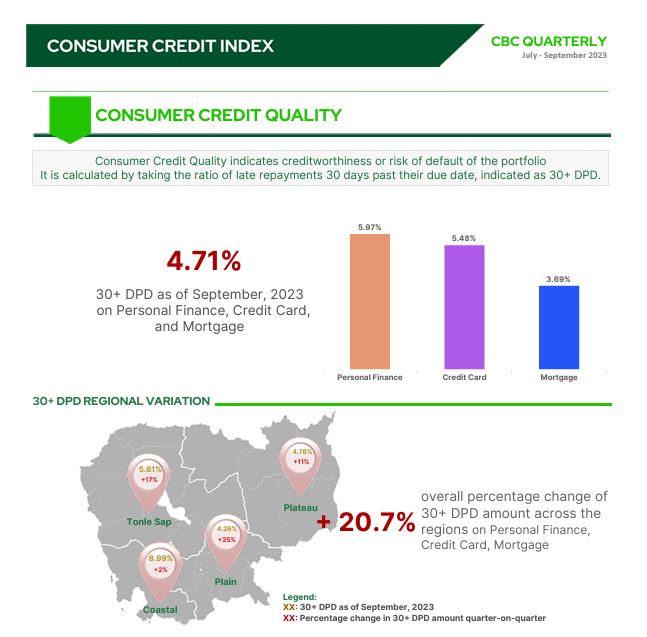

Cambodia’s consumer credit sector continued to reach new heights in the third quarter of 2023, with the total outstanding loan balance swelling to $14.93 billion. This growth, however, comes hand-in-hand with a 20% hike in overdue payments from July to September this year totaling 4.71%, highlighting potential risks looming in the horizon of the credit market, according to data from Credit Bureau of Cambodia.

Consumer credit is defined as personal debt taken and split into three sectors personal finance, mortgage loans, and credit cards. The overall loan balance saw a modest 1.00% increase from the previous quarter, affirming the continued confidence of Cambodian consumers in leveraging credit facilities. The number of consumer loan accounts also witnessed a 1.78% increase, bringing the total to approximately 1.68 million across the country.

Rising Tide of Overdue Payments

A concerning trend is the increase in the ratio of 30+ Days Past Due (DPD) to 4.71%, marking a significant rise from the 3.96% recorded in the second quarter of 2023. This metric, which measures loan accounts with payments overdue by over a month, reflects on the emerging credit risks and borrowers’ financial stress.

The sharpest rise in overdue payments was observed in the Plain region, which saw a 25% escalation, followed by the Tonle Sap, Plateau, and Coastal regions. This uptick in late repayments suggests a potential ripple effect that could affect the health of the overall financial sector if the trend persists.

Despite the concerning rise in overdue payments, the distribution of loan types remained relatively stable. Mortgage loans, despite representing only 12.04% of the total number of loan accounts, accounted for over half of the total outstanding balance, indicating a substantial average loan size in the property sector. Conversely, personal finance loans, while making up a substantial 79.80% of loan accounts, represented just under 44% of the total loan balance.

Credit Market Dynamics

The increase in consumer credit applications, which rose by 11% overall, underscores the continued demand for credit. This was particularly evident in the Personal Finance and Credit Card sectors, which saw applications climb by 16% and 25%, respectively. In contrast, Mortgage Applications saw a decline by 29%, reflecting a shift in consumer borrowing preferences.

“The demand for consumer credit in terms of both the number and amount of applications has increased. Consumer credit performance was positive in terms of both the number of loan accounts and loan balance this quarter,” said Mr. Oeur Sothearoath, CEO of CBC. He cautioned, however, that “loan quality dropped with an increase in the 30+ DPD ratio from 3.96% in the second quarter of 2023 to 4.71% in this quarter.”

Short-Term Market Outlook

Rapidly increasing overdue payments may serve as a cautionary indicator for banks and financial institutions to monitor their credit portfolios closely. It emphasizes the importance of robust credit risk management practices in an environment where consumer credit is expanding.

Industry leaders have emphasized the importance of incorporating data analytics, digitalization, and financial literacy into the debt collection process. Such advancements are critical in reducing loan losses, which otherwise pose a threat to the overall health of a bank’s balance sheet.

The final quarter of 2023 and first half 2024 will be critical in determining whether the market can balance continued growth in consumer credit with the financial health of borrowers, a balancing act that will be key to maintaining the stability and growth of Cambodia’s economy.