Brian Badzmierowski

The real estate sectors in Phnom Penh, Siem Reap, and Sihanoukville remain subdued due to the lingering effects of the pandemic, but there’s hope for a turnaround in the medium to long-term future, according to a recent Knight Frank publication.

“With quarantine restrictions lifted at the beginning of November, there was a notable uptick in activity in the real estate and construction sector during H2 2021 as business sentiment turned cautiously optimistic,” Knight Frank Country Head Ross Wheeble said.

However, some sectors will take longer to recover than others.

Globally, the hospitality and retail sectors have been the most affected by Covid, and Phnom Penh is no exception.

While the government’s full reopening of the economy in November 2021 triggered a small uptick in spending, the retail sector is still struggling.

Reduced footfall compared to pre-pandemic levels and a year-on-year 11 percent increase of retail space in the second half of 2021 won’t ease the sector’s struggles in the short term.

“Whilst there is optimism for retailers over the outlook for Cambodia’s retail sector, there is a clear supply-demand imbalance, with retail supply set to more than double by 2025 if all future projects complete as scheduled,” Knight Frank said in its second-half 2021 report.

Retail supply is expected to increase by 129 percent by 2025, with 75 percent located in the capital’s suburbs. On a positive note, the arrival of H&M in Cambodia was celebrated by Knight Frank.

“H&M is the perfect fit for the local market in terms of price point and branding, and also signals to other global fast-fashion retailers that the Cambodian market is ready for its next stage of evolution,” the real estate firm said.

On the rise of e-commerce, Wheeble said it has mostly affected the food and beverage industry and that on the whole, many consumers in the market still prefer to shop at brick-and-mortar stores, especially when it comes to clothes.

Furthermore, he said, the steady rise in disposable income of Cambodia’s middle class will help the retail sector as this rising class becomes more brand-aware and seeks higher-quality goods.

To read more about the Phnom Penh office rental reduction click here.

Beaten down by a lack of tourists, the hotel sector in the capital continued to suffer during the second half of 2021.

The lifting of quarantine periods for incoming travelers last November helped matters, as December saw a 65 percent increase in tourists from the year before. This helped occupancy rates rise to 15.8 percent from 8.3 percent during the month.

In the medium to long term, the sector is expected to bounce back buoyed by the lifting of travel restrictions and Cambodia’s hosting of the 2023 SEA Games. The outlook looks promising with the potential return of tourists and an uptick in domestic demand due to increases in disposable income.

Chamkarmon District will add 67 percent of the future supply of hotel rooms, largely due to the expected completion of the 3,000-room Naga 3.

Living and Working Spaces

In the serviced apartment sector, occupancy increased to 58 percent during the second half of 2021, but landlords are still facing pressure to provide more flexible options to tenants. The sector has yet to recover from the absence of expatriates and the decreased demand triggered by the pandemic.

International serviced apartment operators, however, are holding out hope for the sector, according to Knight Frank. Several operators are considering entering the market, joining The Ascott Limited, which is currently developing its Leedon Heights project in Sen Sok.

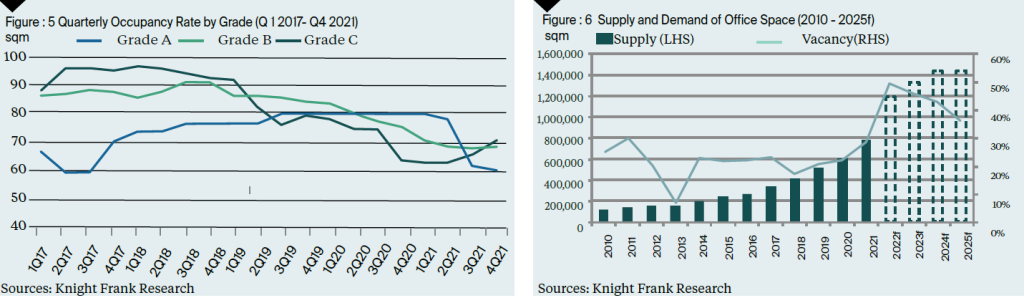

There remains an oversupply of office space in the capital with more office buildings scheduled to be completed in 2022. This creates an ideal situation for smaller businesses looking for office space and puts pressure on landlords to provide more flexible rates.

Office space increased by 161 percent year-on-year in the second half of 2021, mostly in the form of Grade A stratified office buildings. By 2024, the expected supply of office space is expected to rise by 84 percent, Knight Frank indicated.

While leasing activity increased slightly during the second half of 2021, prices remained competitive as landlords vied to attract new tenants and retain current tenants.

Nine new condominium projects were completed in Phnom Penh during the second half of 2021. The average selling price experienced a slight decline from 2020 prices, but Knight Frank’s overall outlook for the condominium sector remains positive.

About 23 percent of future condominium developments will be located in Sen Sok District, a key development zone as Phnom Penh sprawls to the suburbs.

“For a developing country, Cambodia is looking at a higher sales rate from condominium developments and a promising market in the upcoming future. It is a matter of timing, as both developers and buyers are closely eyeing the potential returns from their investments,” Knight Frank reported.

The landed housing sector represents a source of optimism in the real estate sector. During the second half of 2021, 2,706 units were added, with Sen Sok capturing 22 percent of this market supply.

Knight Frank noted that the average sales rate for these projects was 23 percent upon launch, an encouraging sign for the sector.

Selling prices raised slightly compared to 2020 and rental rates remained consistent thanks to domestic and expatriate demand. According to Knight Frank, the domestic demand combined with foreign developers entering the market paints a bright future for the sector.

The future of Siem Reap and Sihanoukville

Knight Frank also looked at Siem Reap and Sihanoukville in its report, two cities facing real estate woes for different reasons. While the real estate situation has yet to meaningfully improve, there are indicators that the medium and long-term futures of both cities represent opportunities for investors and developers.

In Siem Reap, the problems plaguing Phnom Penh were intensified because the province heavily relied on tourism before the pandemic arrived.

While tourists have steadily been increasing since last November, it will take a long time for the retail and hospitality sectors to recover.

On the bright side, government initiatives will help transform the tourist city into a more multi-dimensional offering.

The 38-road construction project, part of the Siem Reap Tourism Development Master Plan 2020-2035, is helping to beautify and upgrade the city while increasing investment in the real estate sector.

A wait-and-see approach is being taken by many in the city with several businesses in the hospitality and retail sectors already temporarily or permanently shuttered.

To read more about the ongoing delay of Capital Gains Tax due to COVID click here.

This was almost entirely due to tourism drying up, which decreased 97.3 percent year-on-year in 2021. When tourism does return, the improvements being made in Siem Reap should help spur its economy in the long term.

“As a consequence [of the improvements], Siem Reap’s tourism sector, particularly hospitality, is anticipated to grow and attract more foreign tourists in the medium and long run, as well as more investment,” Knight Frank said.

While prices remain subdued, the landed housing sector in Siem Reap proved resilient in 2021, adding 515 units between four projects, increasing the stock by 20 percent compared to 2020.

In the near future, landed housing units are expected to jump to 4,564 in Siem Reap, a 78 percent increase from the current available stock.

After suffering the impact of the online gambling ban in 2019 and a recent decline in investment from China that has led to frozen projects, Sihanoukville is undergoing a major overhaul as well.

Increased infrastructure and a re-division of the city into different blocks should help reinvigorate the once quiet seaside city into a desirable destination for both tourists and investors.

“The city has been divided into zones covering tourism, manufacturing, finance, and agri-industries in a bid to diversify its economy and attract investment for multiple source markets,” Knight Frank reported.

To read more about the recently listed property developer JSLand on the local stock market click here.

This transformation will be aided by infrastructure improvements, such as 37 new roads, including a coastal road that will connect Otres with the international airport.

The government plans on turning the city into a diverse economic hub and will consult with the Urban Planning and Design Institute of Shenzhen to inform its master plan.

The “Sihanoukville for all: Promoting Smart, Sustainable, and Inclusive City” project, meanwhile, will help rebuild the city’s reputation as a tourism destination and a forward-thinking city. The project is supported by UN-HABITAT, UN Human Rights, and the UN Trust Fund for Human Security.

The current situation isn’t ideal with an oversupply and unfinished projects, but the long-term prospects look good.

“Planned to be a major gateway city to Cambodia in the future, as well as a smart city, the long-term prospects [of Sihanoukville] are promising, following the return of expatriates and foreign investors,” Knight Frank said.

Wheeble added: “For me, Sihanoukville has better long-term potential than Siem Reap, which is purely tourism-driven at the moment. Sihanoukville has much more industry and a more diversified economy.”